Catalyst Biotech Luglio 2026

Una griglia pulita per homepage con i principali titoli biotech e healthcare negoziabili negli Stati Uniti e date FDA/PDUFA confermate. Nessun link ai singoli report: per la versione .eu restano solo i collegamenti generali al calendario e al blog.

Merlintrader key watchlist

Nota sulla pulizia dei dati

Esclusi: società private, record non negoziabili/quotati negli USA, congressi senza ticker diretto, trial con sola finestra mensile, record AI-detected senza giorno confermato, eventi già decisi come $CORT e date non appartenenti a luglio come $VRDN.

Daily Briefing – 23 giugno: ACHV riceve CRL FDA senza deficiency cliniche, FedEx riporta oggi, Micron è il test AI di domani, oil relief regge ma Hormuz resta fragile

Il briefing .eu del 23 giugno va letto come una mappa di conferma, non più come semplice riapertura di lunedì. La novità più importante è biotech: Achieve Life Sciences ha ricevuto una Complete Response Letter per cytisinicline. La società indica deficiency legate a un impianto di produzione terzo e a final labeling incompleto, ma senza deficiency FDA su efficacia clinica o sicurezza clinica. Questo cambia ACHV da “post-PDUFA in attesa” a storia CRL/resubmission. Sul macro, il petrolio resta in modalità relief mentre il mercato monitora il ritorno dei flussi nello Strait of Hormuz dopo i colloqui USA-Iran, ma il quadro resta fragile. FedEx riporta oggi dopo la chiusura e misura economia reale, freight, parcel, costi e trade flows. Micron riporta domani e diventa il test più pulito su AI memory, HBM e semiconductor momentum. Il 25 giugno arriva il PCE USA, il dato preferito dalla Fed per leggere l’inflazione.

- ACHV— Achieve Life Sciences ha ricevuto una Complete Response Letter per cytisinicline. Il punto chiave è la qualità del CRL: deficiency produttive presso un manufacturing facility terzo e final labeling incompleto, ma nessuna deficiency indicata dalla società su efficacia clinica o sicurezza clinica.FDA CRL

- ACHV— La lettura cambia completamente: non è più corretto scrivere “in attesa di chiarezza ufficiale”. Ora è un CRL confermato con possibile percorso di resubmission. Il mercato guarderà timing Q4 2026, Adare come manufacturer, cash runway, dilution risk e possibilità di preservare il lancio nel primo semestre 2027.Resubmission

- Hormuz / Iran— Il tema del giorno resta sollievo, non normalizzazione completa. Il petrolio scende mentre gli investitori monitorano il ripristino dei flussi nello Strait of Hormuz dopo i colloqui USA-Iran, ma basta poco per riaccendere oil, energia, difesa e dollaro.Geopolitics

- Europa / STOXX— Le borse europee leggono un mix più favorevole ma ancora prudente: oil relief aiuta travel e consumi, la pressione sull’inflazione si raffredda, ma energia e difesa restano sensibili a qualsiasi nuova headline su Hormuz, Iran o shipping risk.Europe

- Oil / Brent / WTI— Brent e WTI restano sotto i picchi di stress recente. Questo aiuta airlines, cruises, consumi e inflation relief. La vera domanda non è solo il prezzo spot, ma la durata del relief: se i flussi Hormuz reggono, travel respira; se il rischio torna, energy riprende sponsorship.Oil Watch

- SPY / QQQ— La seduta USA deve confermare se il risk appetite è sano. SPY serve per la breadth, QQQ per growth/AI, SOXX per leadership semiconductor e IWM per capire se il rally resta concentrato o prova davvero ad allargarsi.US Tape

- MRVL / FLEX— Marvell e Flex sono entrate nello S&P 500 dal 22 giugno. Oggi non è più solo inclusion day: è follow-through. Il test è capire se i flussi passivi lasciano supporto stabile o se arriva il classico sell-the-event dopo l’assorbimento dei flussi obbligati.Index Follow-Up

- MRVL— Marvell resta la più tematica delle due inclusioni perché combina index-flow, AI networking, custom silicon e data-center infrastructure. La lettura migliore sarebbe tenuta del titolo anche dopo l’evento e conferma del tape semiconductor prima di Micron.AI / Index

- FLEX— Flex resta interessante come proxy industrial tech, electronics manufacturing e supply chain per server/data center. Il rischio principale è che parte del movimento sia già stata anticipata prima dell’ingresso nell’indice.Industrial Tech

- FDX— FedEx pubblica il Q4 FY26 oggi, 23 giugno. Il mercato userà il call per leggere domanda logistica, volumi parcel/freight, pricing, cost control, trade flows e aggiornamenti sulla separazione FedEx Freight. È il test “economia reale” prima del test AI di Micron.Earnings Today

- MU— Micron è il controllo qualità del rally AI. Gli earnings del 24 giugno diventano il test su HBM, memoria AI, pricing DRAM/NAND, data-center demand, margini e guidance. Se MU conferma domanda forte, il basket AI semis può restare leader; se delude, il mercato può diventare molto più selettivo.AI Semis

- NVDA / AVGO / AMD / ARM— Il paniere AI semiconductor resta il cuore del growth trade. Nvidia guida la narrativa, Broadcom controlla custom silicon/networking, AMD misura il secondo livello del trade e Arm resta un proxy architetturale. Questa settimana servono earnings confirmation, non solo entusiasmo tematico.AI Basket

- SPRO / GSK— SPRO/GSK restano da seguire dopo l’approvazione FDA di Utebzi, tebipenem pivoxil, per adulti con complicated UTI inclusa pyelonephritis e opzioni orali limitate o assenti. La storia ora passa da rischio regolatorio a label, launch timing, stewardship, milestones e royalties.FDA Approval

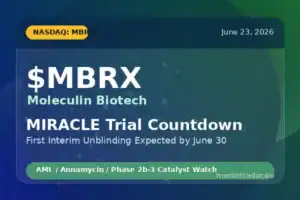

- VRDN— Viridian resta il prossimo catalyst regolatorio pulito: veligrotug è sotto FDA Priority Review con PDUFA target action date al 30 giugno 2026 per thyroid eye disease. Dopo SPRO e ACHV, la biotech tape resta concentrata su date precise e outcome verificabili.PDUFA Watch

- COGT / XBI— Cogent resta un follow-through post-data, mentre XBI è il vero termometro del risk appetite biotech. Il settore non è in modalità “tutto sale”: funziona meglio su catalyst chiari, dati verificabili e tassi meno ostili.Biotech

- ACN— Accenture resta il warning principale sull’AI services trade: il mercato continua a distinguere tra infrastruttura AI, chip, data center e consulenza/IT services. Non tutto ciò che contiene “AI” beneficia allo stesso ritmo.AI Services

- SPCX / RKLB / LUNR / PL— Lo space trade resta in digestione dopo il momentum recente. SpaceX è ancora il termometro retail, ma la parte pubblica del paniere deve mostrare forza propria: Rocket Lab, Intuitive Machines e Planet Labs non possono vivere solo di simpatia tematica.Space

- PCE 25 giugno— Il prossimo macro gate è il PCE inflation del 25 giugno, il dato preferito dalla Fed. Dopo la volatilità del petrolio e lo stress geopolitico, il numero pesa ancora di più: dato morbido aiuta risk assets; dato caldo rafforza higher-for-longer, dollaro e pressione sui multipli.Inflation

- PMI / Housing / Durable Goods— La settimana porta anche flash PMI, new-home sales e durable goods. Sono dati meno “sexy” dei chip, ma servono a capire se l’economia USA è davvero resiliente o se il rally resta troppo dipendente da AI e oil relief.Macro Data

- Fed / Dollaro— La Fed resta il freno silenzioso. Dollaro forte e lettura hawkish aumentano il costo del capitale e possono comprimere small caps, biotech speculative e long-duration growth. Il mercato può restare costruttivo, ma non è un risk-on senza condizioni.Rates

- Rebalance— I ribilanciamenti creano rumore tecnico. MRVL/FLEX, flussi ETF, volumi di apertura/chiusura e posizionamento possono distorcere i movimenti di breve periodo rispetto ai fondamentali.Flows

- Credit monitor— LQD e HYG restano segnali chiave. Un rally equity senza conferma del credito è più fragile; un credito stabile rende più credibile la continuazione del risk-on.Credit

- Europe read— Per l’Europa il mix è delicato: oil relief aiuta travel e consumi, ma riduce il premio sulle energy; healthcare resta difensivo; banche italiane e industriali dipendono da tassi, spread e rischio globale.Europe

Daily Briefing – June 23: ACHV Gets FDA CRL With No Clinical Deficiency, FedEx Reports Today, Micron Becomes Tomorrow’s AI Memory Test, Oil Relief Holds but Hormuz Remains Fragile

The June 23 briefing for the .eu site should be read as a confirmation map, not a Monday reopen preview. The most important biotech update is now clear: Achieve Life Sciences has received a Complete Response Letter for cytisinicline. The company says the CRL cites deficiencies at a third-party manufacturing facility and incomplete final labeling, while no clinical efficacy or clinical safety deficiencies were identified. That changes ACHV from a post-PDUFA awaiting-clarity watch into a confirmed CRL/resubmission-path story. On the macro side, oil is still trading with a relief tone as investors monitor restoring flows through the Strait of Hormuz after U.S.-Iran peace talks, but the setup remains fragile. FedEx reports today after the close and checks freight, parcels, cost control and real-economy demand. Micron reports tomorrow and becomes the cleanest AI-memory, HBM and semiconductor-momentum test. The June 25 PCE report remains the Fed’s key inflation gate.

- ACHV— Achieve Life Sciences received a Complete Response Letter for cytisinicline. The key point is the type of CRL: third-party manufacturing deficiencies and incomplete final labeling, with no clinical efficacy or clinical safety deficiencies identified by the company.FDA CRL

- ACHV— The trading read changes completely: it is no longer correct to describe the story as awaiting official clarity. It is now a confirmed CRL with a potential resubmission path. The market will focus on Q4 2026 timing, Adare as manufacturer, cash runway, dilution risk and whether a first-half 2027 launch scenario can remain credible.Resubmission

- Hormuz / Iran— Today’s theme remains relief, not full normalization. Oil is lower as investors monitor restoring flows through the Strait of Hormuz after U.S.-Iran peace talks, but the risk can still quickly reprice oil, energy, defence and the dollar.Geopolitics

- Europe / STOXX— European shares are reading a more favorable but still cautious mix: oil relief helps travel and consumption, inflation pressure cools, but energy and defence remain sensitive to any new headline on Hormuz, Iran or shipping risk.Europe

- Oil / Brent / WTI— Brent and WTI remain below recent stress highs. That helps airlines, cruises, consumption and inflation relief. The real question is durability: if Hormuz flows hold, travel can breathe; if risk returns, energy regains sponsorship.Oil Watch

- SPY / QQQ— The U.S. session needs to confirm whether risk appetite is healthy. SPY checks breadth, QQQ checks growth/AI, SOXX checks semiconductor leadership and IWM shows whether the rally remains narrow or starts to broaden.US Tape

- MRVL / FLEX— Marvell and Flex entered the S&P 500 effective June 22. Today is no longer just inclusion day; it is follow-through. The test is whether passive flows leave durable support or whether the move becomes a classic sell-the-event after required flows are absorbed.Index Follow-Up

- MRVL— Marvell remains the more thematic inclusion because it combines index-flow, AI networking, custom silicon and data-center infrastructure. The best read would be post-event support plus a stable semiconductor tape into Micron.AI / Index

- FLEX— Flex remains useful as an industrial tech, electronics manufacturing and server/data-center supply-chain proxy. The main risk is that part of the move was already pulled forward before index entry.Industrial Tech

- FDX— FedEx reports Q4 FY26 today, June 23. The market will use the call to read logistics demand, parcel/freight volumes, pricing, cost control, trade flows and FedEx Freight separation updates. It is the real-economy test before Micron’s AI test.Earnings Today

- MU— Micron is the quality-control test for the AI rally. The June 24 earnings report becomes a check on HBM, AI memory, DRAM/NAND pricing, data-center demand, margins and guidance. If MU confirms strength, AI semis can keep leadership; if it disappoints, the market can become much more selective.AI Semis

- NVDA / AVGO / AMD / ARM— The AI semiconductor basket remains the heart of the growth trade. Nvidia anchors the narrative, Broadcom checks custom silicon/networking, AMD measures second-line appetite and Arm remains an architecture proxy. This week needs earnings confirmation, not just theme enthusiasm.AI Basket

- SPRO / GSK— SPRO/GSK remain relevant after FDA approval of Utebzi, tebipenem pivoxil, for adults with complicated UTIs including pyelonephritis and limited or no oral alternatives. The story has shifted from regulatory risk to label, launch timing, stewardship, milestones and royalties.FDA Approval

- VRDN— Viridian remains the next clean regulatory catalyst: veligrotug is under FDA Priority Review with a June 30, 2026 PDUFA target action date in thyroid eye disease. After SPRO and ACHV, the biotech tape remains focused on dated, verifiable outcomes.PDUFA Watch

- COGT / XBI— Cogent remains a post-data follow-through name, while XBI is the broader biotech risk-appetite gauge. The sector is not in an “everything works” regime; it works best through clear catalysts, verifiable data and less hostile rates.Biotech

- ACN— Accenture remains the key warning for the AI-services trade: the market continues to separate AI infrastructure, chips and data centers from consulting and IT services. Not everything with “AI” benefits at the same speed.AI Services

- SPCX / RKLB / LUNR / PL— The space trade remains in digestion mode after recent momentum. SpaceX is still the retail thermometer, but the public basket needs its own relative strength: Rocket Lab, Intuitive Machines and Planet Labs cannot rely only on theme sympathy.Space

- PCE June 25— The next macro gate is the June 25 PCE inflation release, the Fed’s preferred gauge. After oil volatility and geopolitical stress, the number matters even more: a soft print helps risk assets; a hot print reinforces higher-for-longer, the dollar and pressure on multiples.Inflation

- PMI / Housing / Durable Goods— The week also brings flash PMIs, new-home sales and durable goods. They are less exciting than chips, but they matter for judging whether the U.S. economy is genuinely resilient or still too dependent on AI and oil relief.Macro Data

- Fed / Dollar— The Fed remains the quiet brake. A strong dollar and hawkish policy read raise the cost of capital and can compress small caps, speculative biotech and long-duration growth. The market can stay constructive, but this is not unconditional risk-on.Rates

- Rebalance— Index rebalancing creates technical noise. MRVL/FLEX, ETF flows, opening/closing volumes and positioning can distort short-term moves versus fundamentals.Flows

- Credit monitor— LQD and HYG remain key confirmation signals. An equity rally without credit support is more fragile; stable credit makes risk-on more credible.Credit

- Europe read— For Europe the mix is delicate: oil relief helps travel and consumption but reduces the premium on energy; healthcare stays defensive; Italian banks and industrials depend on rates, spreads and global risk.Europe