Humacyte (Nasdaq: $HUMA): la presentazione V012 rafforza la storia nell’accesso dialitico, ma diluizione ed esecuzione restano il vero test

La storia di Humacyte nel giugno 2026 è ormai andata oltre il primo titolo sui dati V012. La società ha pubblicato e presentato un quadro più completo dello studio Phase 3 nelle pazienti donne in dialisi, includendo endpoint secondari di efficacia, dati sulle infezioni, dettagli di safety e il percorso previsto verso una supplemental BLA. L’aggiornamento clinico è più solido di un semplice comunicato top-line, ma la storia del titolo resta complicata dall’offerta azionaria da 50 milioni di dollari appena prezzata, dal lancio ancora iniziale di Symvess, dai ricavi ancora bassi e da un bilancio che richiede disciplina.

Prossimi punti da monitorare dopo l’update del 15 giugno

Il catalyst V012 non è più pendente. I dati top-line sono stati annunciati il 10 giugno 2026, mentre l’aggiornamento più dettagliato è stato pubblicato il 15 giugno dopo la presentazione al Vascular Annual Meeting della Society for Vascular Surgery. Da qui in avanti, i punti da seguire sono l’investor event fissato per il 15 giugno alle 5:00 p.m. ET, eventuali ulteriori commenti del management sul pacchetto per la supplemental BLA, i dettagli finali sull’aumento di capitale di giugno e sull’opzione agli underwriter, la runway aggiornata dopo il finanziamento e il deposito della supplemental BLA previsto dalla società nella seconda metà del 2026.

Executive Summary

Humacyte non è più una semplice storia da “evento dati”. La società ha superato il catalyst V012 di giugno, ha comunicato un interim win statisticamente significativo in Phase 3, ha presentato dati più completi allo SVS VAM e ha aggiunto abbastanza contesto su endpoint secondari e safety da rendere più sostanziale la tesi nell’accesso dialitico. Ma il mercato ha ricevuto anche un promemoria molto chiaro: il progresso clinico non elimina il rischio finanziario nelle small-cap biotech. L’offerta da 50 milioni di dollari in azioni ordinarie, prezzata a 1,05 dollari per azione, arriva accanto alla vittoria clinica e questa combinazione definisce il tape attuale di HUMA.

Il punto clinico più importante resta semplice. Nello studio Phase 3 V012, le donne trattate con l’acellular tissue engineered vessel di Humacyte, o ATEV, hanno registrato in media 220 giorni senza catetere nel primo anno, rispetto a 129 giorni per le pazienti trattate con autologous AV fistula, l’attuale standard of care. Si tratta di un vantaggio medio di 91 giorni, con significatività statistica riportata da Humacyte pari a p=0.00070. In un contesto di accesso per emodialisi, dove la dipendenza dal catetere può significare rischio infettivo, complicanze e ripetuti interventi, l’endpoint è intuitivo sia per investitori sia per clinici.

L’aggiornamento del 15 giugno conta perché aggiunge profondità oltre al titolo principale. Humacyte ha comunicato ulteriori misure secondarie di efficacia: i giorni senza catetere a sei mesi sono stati in media 88 con ATEV contro 32 con AV fistula; la functional patency a 12 mesi è stata in media 250 giorni con ATEV contro 152 con AV fistula; la secondary patency a sei mesi è stata 87,5% con ATEV contro 65,0% con AV fistula; e la secondary patency a dodici mesi è stata 77,5% con ATEV contro 62,5% con AV fistula. Su quest’ultimo punto, però, il p-value riportato è p=0.16, quindi il dato va descritto come vantaggio numerico, non come risultato statisticamente significativo.

Anche il dettaglio sulla safety è diventato più utile. Humacyte ha riportato circa sei infezioni per 100 patient-years nel gruppo ATEV contro 23 infezioni per 100 patient-years nel gruppo AV fistula. La società ha inoltre indicato che nessuna infezione nel gruppo ATEV era collegata all’accesso oggetto dello studio, contro tre infezioni di questo tipo nel gruppo AV fistula, e che non si sono verificate rotture in nessuno dei due gruppi. Gli eventi avversi seri sono stati riportati a 1,73 per ATEV contro 4,77 per AV fistula su base patient-years aggiustata. Gli eventi avversi di speciale interesse sono stati 2,71 per ATEV contro 3,88 per AV fistula; gli eventi trombotici 0,75 per ATEV contro 0,51 per AV fistula, con il 75,0% dei casi di trombosi ATEV risolto con successo contro il 37,5% per AV fistula; e gli eventi stenotici 1,62 per ATEV contro 2,29 per AV fistula.

Il percorso regolatorio è ora più visibile, ma non completo. Humacyte prevede di depositare una supplemental Biologics License Application presso la FDA nella seconda metà del 2026. L’indicazione target pianificata riguarda adulti con end-stage kidney disease a maggiore rischio di fallimento della maturazione di AV fistula. Questo perimetro è importante perché suggerisce che Humacyte non stia semplicemente cercando una label generica nell’“accesso dialitico”; sta cercando di posizionare ATEV dove la fistola standard ha più probabilità di fallire o di lasciare il paziente troppo a lungo dipendente dal catetere.

La storia finanziaria è il contrappeso. Le vendite commerciali di Symvess nel Q1 2026 sono state 0,5 milioni di dollari, pari a 29 unità, rispetto a 0,1 milioni e cinque unità nel Q1 2025. È un progresso, ma resta una base di ricavi molto piccola rispetto alle ambizioni di R&D, manufacturing, commercializzazione e regolatorio della società. Nel Q1 2026 le spese R&D sono state 19,5 milioni di dollari, le G&A 7,9 milioni e la perdita netta 17,6 milioni. Cash, cash equivalents e restricted cash erano 48,9 milioni al 31 marzo 2026, prima dei proventi dell’offerta di giugno.

La lettura pulita è questa: HUMA oggi ha una storia clinica e regolatoria più forte rispetto a prima del readout V012, ma la storia azionaria resta sporca. Il titolo deve assorbire la diluizione, dimostrare esecuzione commerciale, depositare la supplemental BLA, attraversare il processo FDA e provare che Symvess e ATEV possano diventare più di una piattaforma scientificamente interessante. I buoni dati clinici hanno comprato credibilità a Humacyte. Non le hanno dato un pass gratuito.

Cosa è cambiato con l’aggiornamento del 15 giugno 2026

Il comunicato del 10 giugno ha dato al mercato il risultato top-line di V012. L’aggiornamento del 15 giugno fornisce invece il quadro più completo della presentazione. La differenza è importante. Nel biotech, un p-value da titolo può muovere un’azione per qualche ora, ma un dataset più completo decide se la storia può sopravvivere oltre la prima reazione di trading. Per Humacyte, l’update del 15 giugno rafforza la narrativa clinica perché mostra che il vantaggio non era limitato a un singolo numero isolato.

L’endpoint primario era già noto: ATEV ha superato AV fistula sui catheter-free days nell’analisi interim prespecificata dei primi 80 pazienti che avevano completato 12 mesi di follow-up. L’aggiornamento presentato il 15 giugno conferma quel risultato e aggiunge ulteriori endpoint clinicamente rilevanti. Un prodotto progettato per sostituire o integrare le opzioni standard nell’accesso emodialitico non ha bisogno soltanto di un numero positivo. Ha bisogno di un pattern coerente tra riduzione dell’uso del catetere, patency, infezioni, complicanze correlate all’accesso e durata.

Il nuovo aggiornamento di Humacyte punta in quella direzione, con una precisazione importante: gli investitori non dovrebbero trattare tutti i numeri allo stesso modo. L’endpoint dei catheter-free days a sei mesi, la functional patency a dodici mesi e la secondary patency a sei mesi hanno mostrato p-value forti a favore di ATEV. La secondary patency a dodici mesi favoriva numericamente ATEV, ma è stata riportata con p=0.16; quindi va descritta come vantaggio numerico e non come risultato statisticamente significativo. Questa distinzione è essenziale per la credibilità, soprattutto in un report destinato a lettori biotech esigenti.

| Misura V012 | ATEV | AV Fistula | p-value riportato | Lettura Merlintrader |

|---|---|---|---|---|

| Giorni medi senza catetere nel primo anno | 220 giorni | 129 giorni | p=0.00070 | Endpoint primario raggiunto; vantaggio medio di 91 giorni clinicamente intuitivo. |

| Giorni senza catetere a sei mesi | 88 giorni | 32 giorni | p=0.00009 | Supporta il beneficio più precoce nella riduzione della dipendenza da catetere. |

| Functional patency a 12 mesi | 250 giorni | 152 giorni | p=0.00057 | Importante perché la durata dell’accesso conta sul piano clinico e commerciale. |

| Secondary patency a sei mesi | 87,5% | 65,0% | p=0.0013 | Segnale favorevole sulla patency nel breve periodo. |

| Secondary patency a dodici mesi | 77,5% | 62,5% | p=0.16 | Numericamente favorevole, ma non statisticamente significativo in base al p-value riportato. |

Il modo più utile per leggere l’update non è dire che “HUMA ha annunciato di nuovo gli stessi dati”. Sarebbe una lettura superficiale. La cornice corretta è che Humacyte ora dispone di un argomento clinico più completo per il pacchetto della supplemental BLA. Il risultato top-line del 10 giugno ha stabilito che V012 ha raggiunto l’endpoint primario. Il comunicato del 15 giugno mostra quanto il risultato sembri estendersi ad altre misure chiave dell’accesso dialitico. Questo conta perché FDA review, adozione dei medici e discussioni con i payer raramente dipendono da un solo indicatore isolato.

HUMA non deve più essere inquadrata come una storia “in attesa del catalyst V012 dell’11 giugno”. Il catalyst è già avvenuto. La storia è ora post-readout e post-presentazione. La prossima fase riguarda l’esecuzione della supplemental BLA, il rischio FDA, il perimetro della label, la traduzione commerciale e il bilancio dopo il finanziamento da 50 milioni di dollari.

Il risultato V012 spiegato in modo semplice

I pazienti in emodialisi hanno bisogno di un accesso affidabile al flusso sanguigno. L’accesso deve permettere al sangue di uscire dal corpo, passare attraverso la macchina per dialisi e rientrare in sicurezza. L’approccio standard è spesso una fistola artero-venosa autologa, dove il chirurgo collega un’arteria e una vena. In teoria le fistole sono durevoli e preferibili. Nella pratica possono richiedere tempo per maturare, possono non maturare affatto e possono costringere i pazienti a restare dipendenti da cateteri.

I cateteri sono problematici perché possono essere associati a infezioni del sangue e altre complicanze. Più a lungo un paziente resta dipendente dal catetere, più tempo rimane esposto a quel rischio. Per questo i catheter-free days non sono un endpoint astratto. Sono facili da capire: più giorni senza catetere significano meno tempo con un catetere.

L’ATEV di Humacyte è progettato come vaso umano bioingegnerizzato off-the-shelf. L’idea è fornire un condotto vascolare che i chirurghi possano usare quando il paziente ha bisogno di accesso e quando le opzioni convenzionali potrebbero non funzionare abbastanza bene. Non è un graft sintetico nel senso semplice del termine; deriva da cellule umane coltivate e viene poi processato in un vaso acellulare pensato per essere impiantabile universalmente. L’obiettivo della piattaforma è combinare disponibilità simile a un dispositivo e caratteristiche biologiche di integrazione.

In V012, il confronto primario era tra ATEV e AV fistula in donne in dialisi. Il focus sulla popolazione femminile è importante. Humacyte ha sottolineato più volte che le donne possono avere maggiori difficoltà di maturazione della fistola rispetto agli uomini, anche per dimensioni dei vasi e caratteristiche anatomiche. La popolazione target dello studio ha quindi una logica clinica chiara: se l’accesso standard con fistola fallisce più spesso o matura meno affidabilmente in certi pazienti, un’alternativa off-the-shelf può avere un ruolo più difendibile.

Il risultato riportato è abbastanza chiaro per un pubblico ampio. Le pazienti ATEV hanno registrato in media 220 giorni senza catetere rispetto a 129 giorni per AV fistula nel primo anno. Il vantaggio medio di 91 giorni è il cuore della storia. È ampio, intuitivo e statisticamente significativo. Gli endpoint secondari diffusi il 15 giugno rendono la storia più robusta perché aggiungono contesto su functional patency e secondary patency invece di lasciare gli investitori con un solo numero da comunicato stampa.

Detto questo, il risultato V012 non va confuso con un’approvazione. Un’analisi interim positiva di Phase 3 e una presentazione dettagliata supportano il deposito previsto. Non garantiscono accettazione FDA, priority review, approvazione, linguaggio finale della label, copertura dei payer, adozione dei medici o successo commerciale. La FDA dovrà ancora valutare il pacchetto completo, inclusi efficacia, safety, conduzione dello studio, manufacturing, labeling, benefit-risk, eventuali impegni post-marketing e il rapporto tra V012 e dati precedenti nell’accesso AV come V007.

Perché la popolazione femminile nell’accesso dialitico conta

Uno dei motivi per cui V012 è più interessante di un generico trial sull’accesso vascolare è la popolazione. Le donne in dialisi non sono un sottogruppo casuale scelto per effetto marketing. Rappresentano una popolazione con unmet need elevato, nella quale la maturazione della fistola e la dipendenza da catetere possono essere particolarmente difficili. La stessa Humacyte sostiene che le donne che ricevono accesso AV abbiano bisogni clinici importanti perché le fistole spesso non si sviluppano correttamente, costringendo troppe pazienti a usare cateteri.

Per gli investitori questo ha due implicazioni. La prima, positiva, è che una popolazione più mirata e ad alto rischio può rendere l’argomento clinico e regolatorio più comprensibile. Invece di sostenere che “ATEV dovrebbe sostituire le fistole ovunque”, Humacyte può argomentare che ATEV potrebbe essere particolarmente utile negli adulti con end-stage kidney disease a maggiore rischio di fallimento della maturazione di AV fistula. È un’indicazione più mirata e potenzialmente più difendibile.

La seconda implicazione è più prudente: un’indicazione target richiede anche cautela nella lettura della dimensione di mercato. Una label più piccola e definita può supportare l’adozione in una nicchia ad alto bisogno, ma non significa automaticamente che l’intero mercato dell’accesso emodialitico diventi immediatamente accessibile. L’opportunità commerciale dipenderà dal linguaggio finale della label, dalle linee guida cliniche, dalla confidenza dei medici, dal rimborso, dai processi di acquisto ospedalieri, dalla capacità produttiva e dalla performance real-world.

Questa distinzione conta perché HUMA ha spesso trattato come una storia di piattaforma ampia. La narrativa della piattaforma è potente: trauma, accesso dialitico, peripheral artery disease, coronary artery bypass grafting, chirurgia cardiaca pediatrica, diabete di tipo 1 e altre applicazioni tissutali. Ma la creazione di valore sul mercato pubblico dipenderà probabilmente prima dall’esecuzione in indicazioni concrete. Il trauma vascolare ha dato a Humacyte il primo prodotto approvato dalla FDA. V012 potrebbe sostenere una seconda indicazione importante. La società deve ancora trasformare questi traguardi in ricavi e adozione.

Il setup regolatorio dopo V012

Humacyte ha già un prodotto ATEV approvato dalla FDA nel trauma vascolare. Symvess è indicato negli adulti come condotto vascolare per lesione arteriosa degli arti quando è necessaria una rivascolarizzazione urgente per evitare una perdita imminente dell’arto e quando un graft di vena autologa non è praticabile. Questa approvazione è importante perché Humacyte non è più una biotech puramente pre-commerciale. Ha un prodotto biologico approvato e un lancio commerciale reale.

L’indicazione per accesso emodialitico è separata. Humacyte ha chiarito che, al di fuori dell’indicazione FDA approvata per trauma vascolare degli arti, ATEV resta un prodotto investigazionale e non è approvato per la vendita dalla FDA o da altre autorità regolatorie. Questo punto deve restare visibile in qualsiasi report pubblico, perché i dati V012 supportano un’espansione potenziale, ma non equivalgono a un’approvazione commerciale.

La società ora prevede di depositare una supplemental BLA presso la FDA nella seconda metà del 2026. L’indicazione target attualmente pianificata riguarda adulti con end-stage kidney disease ad aumentato rischio di fallimento della maturazione di AV fistula. Se il filing verrà presentato, la sequenza successiva includerà verifica di accettazione da parte della FDA, assegnazione di una timeline di review, possibili richieste di informazioni, discussioni sulla label, revisione del manufacturing e una decisione regolatoria finale.

La domanda chiave è come la FDA valuterà la totalità delle evidenze. V012 offre a Humacyte un forte dataset interim nelle donne in accesso dialitico. Anche i dati precedenti V007 restano rilevanti, perché Humacyte ha già posizionato il programma di accesso AV come late-stage più ampio. Il pacchetto regolatorio dovrà dimostrare che il profilo beneficio-rischio è favorevole nella popolazione proposta, non soltanto che un endpoint è risultato positivo.

L’update V012 migliora la probabilità che Humacyte possa presentare una supplemental BLA più persuasiva. Non elimina il rischio FDA. Il mercato deve separare “la società ha una storia di filing più forte” da “l’indicazione è già approvata”.

| Tempistica | Evento | Stato | Perché conta |

|---|---|---|---|

| Dicembre 2024 | Approvazione FDA di Symvess nel trauma vascolare degli arti | Completato | Rende Humacyte una biotech commercial-stage con un prodotto ATEV approvato. |

| 10 giugno 2026 | Risultato top-line interim Phase 3 V012 | Completato | ATEV ha raggiunto l’endpoint primario rispetto ad AV fistula sui giorni senza catetere. |

| 15 giugno 2026 | Update dettagliato della presentazione V012 | Completato | Aggiunge endpoint secondari e contesto di safety dopo la presentazione SVS VAM. |

| 15 giugno 2026 alle 5:00 p.m. ET | Investor event su V012 | Programmato | Può fornire ulteriore commento del management su filing strategy, selezione pazienti e implicazioni commerciali. |

| Seconda metà 2026 | Deposito previsto della supplemental BLA | Pendente | Prossimo milestone regolatorio principale per l’indicazione di accesso AV. |

L’offerta azionaria: perché il setup del titolo resta complesso

L’evento non clinico più importante nella storia HUMA è il finanziamento di giugno 2026. Nello stesso giorno in cui Humacyte ha annunciato il risultato positivo V012, ha annunciato anche una public offering. La società ha poi prezzato l’offerta a 47.619.048 azioni ordinarie a 1,05 dollari per azione, per proventi lordi attesi di 50 milioni di dollari prima di sconti, commissioni e altre spese. Gli underwriter hanno ricevuto anche un’opzione di 30 giorni per acquistare fino a ulteriori 7.142.857 azioni allo stesso prezzo pubblico, al netto di sconti e commissioni.

Per questo la reazione del titolo non può essere analizzata solo attraverso la lente clinica. Dal punto di vista scientifico e regolatorio, V012 è stato positivo. Dal punto di vista del mercato dei capitali, gli azionisti hanno dovuto assorbire immediatamente una grande emissione di nuove azioni ordinarie. Nelle small-cap biotech questa combinazione è comune: le società spesso raccolgono capitale sulla forza di un catalyst perché l’evento crea liquidità e perché il successo clinico aumenta il bisogno di finanziare la fase successiva. Ma per gli azionisti esistenti la matematica resta importante.

Il precedente update Merlintrader inquadrava l’offerta base come 47.619.048 nuove azioni. Usando le 222.019.108 azioni ordinarie in circolazione al 23 aprile 2026, record date indicata nell’8-K del 9 giugno, l’emissione base equivale a circa il 21,45% di quel numero di azioni e a circa il 17,66% del semplice totale pro forma di azioni ordinarie dopo l’emissione. Se l’opzione degli underwriter fosse esercitata integralmente, le nuove azioni totali salirebbero a 54.761.905, pari a circa il 24,67% del conteggio alla record date e circa il 19,79% del totale semplice pro forma.

Non è un modello fully diluted. Non include opzioni, warrant, RSU, future vendite ATM, programmi azionari futuri, convertibili o ulteriori finanziamenti. Ma basta a mostrare perché l’offerta conta. Il mercato non sta decidendo solo se V012 fosse clinicamente buono. Sta decidendo se il miglioramento clinico giustifica il nuovo conteggio azionario e se i proventi danno a Humacyte abbastanza runway per eseguire il piano sBLA e commerciale senza tornare subito sul mercato.

| Scenario finanziamento | Nuove azioni | Proventi lordi | Quadro semplice di diluizione |

|---|---|---|---|

| Offerta pubblica base | 47.619.048 azioni | $50,0 milioni prima di sconti, commissioni e spese | Circa 21,45% delle azioni ordinarie alla record date del 23 aprile; circa 17,66% del semplice totale pro forma. |

| Se l’opzione underwriter viene esercitata integralmente | 54.761.905 nuove azioni totali | Circa $57,5 milioni lordi prima di sconti, commissioni e spese | Circa 24,67% delle azioni ordinarie alla record date del 23 aprile; circa 19,79% del semplice totale pro forma. |

| Uso dei proventi | Non applicabile | Proventi netti alla società dopo le spese | Commercializzazione di Symvess, supplemental BLA prevista in emodialisi, pipeline, working capital e finalità corporate generali. |

L’offerta non cancella la vittoria V012, ma cambia il setup del titolo. Il tape HUMA di breve periodo è un tiro alla fune tra una storia clinica più forte e un peso maggiore in termini di share count e diluizione. È esattamente per questo che il commento dell’investor event e la runway aggiornata contano.

Situazione finanziaria, ricavi Symvess e pressione sulla runway

I numeri del Q1 2026 spiegano perché Humacyte abbia raccolto capitale subito dopo il catalyst V012. Le vendite commerciali di Symvess sono aumentate, ma restano piccole. La società ha riportato vendite commerciali di Symvess per 0,5 milioni di dollari, pari a 29 unità, nel Q1 2026, rispetto a 0,1 milioni di dollari e cinque unità nel Q1 2025. L’adozione si muove nella direzione giusta, ma la base di ricavi è ancora minuscola rispetto alla struttura dei costi operativi.

Il fatturato totale è stato 495.000 dollari nel Q1 2026, contro 517.000 dollari nel Q1 2025. Il confronto headline appare stabile o leggermente in calo, ma il mix è cambiato. I ricavi da prodotto sono migliorati, mentre i ricavi da contratto collegati a una collaborazione di ricerca sono diminuiti perché la relativa fase della collaborazione era stata completata. È una distinzione significativa: il business sta diventando più product-driven, ma non ha ancora raggiunto scala commerciale.

Il cost of goods sold è stato 2,0 milioni di dollari nel Q1 2026, contro 0,1 milioni nel Q1 2025. Humacyte ha indicato che solo 0,2 milioni del COGS del Q1 2026 erano collegati alle unità registrate come ricavi di vendita, mentre il resto riguardava principalmente una riserva inventariale da 1,6 milioni e overhead legati a capacità produttiva inutilizzata. È un segnale importante: manufacturing scale e utilization contano. Se Symvess e future indicazioni ATEV cresceranno, la leva operativa potrebbe migliorare. Se i ricavi resteranno lenti, la capacità inutilizzata e l’economia dell’inventario potranno pesare molto.

Le spese R&D sono state 19,5 milioni di dollari nel Q1 2026, in aumento rispetto a 15,4 milioni nel Q1 2025. Humacyte ha attribuito l’aumento soprattutto ai costi dei materiali, principalmente da run produttivi non commerciali collegati a CTEV e a lavori di process improvement pensati per ridurre il cost of goods sold nel tempo. Le G&A sono state 7,9 milioni, sostanzialmente in linea con gli 8,1 milioni dell’anno precedente. La perdita netta è stata 17,6 milioni, rispetto a un utile netto di 39,1 milioni nel Q1 2025, ma il confronto dell’anno precedente era pesantemente influenzato da income non cash legato alla rivalutazione della contingent earnout liability.

Cash, cash equivalents e restricted cash erano 48,9 milioni di dollari al 31 marzo 2026. Humacyte ha anche annunciato a maggio 2026 riduzioni di organico e costi operativi, inclusa la riduzione di circa 45 dipendenti e il rinvio di assunzioni pianificate. La società ha stimato risparmi netti per circa 14,3 milioni durante il resto del 2026, dopo severance e costi collegati. Questa disciplina dei costi conta, ma l’aumento di capitale di giugno mostra che da sola non bastava a rimuovere il rischio finanziario.

| Metrica | Q1 2026 | Q1 2025 | Lettura |

|---|---|---|---|

| Vendite commerciali Symvess | $0,5 milioni / 29 unità | $0,1 milioni / 5 unità | Crescita chiara del prodotto da una base molto piccola. |

| Ricavi totali | $495.000 | $517.000 | Ricavi headline piatti perché la crescita del prodotto è stata compensata da minori ricavi da contratto. |

| Cost of goods sold | $2,0 milioni | $0,1 milioni | Include riserva inventariale e costi da capacità produttiva inutilizzata. |

| Spese R&D | $19,5 milioni | $15,4 milioni | Maggiore spesa collegata anche a manufacturing non commerciale e process improvement. |

| Spese G&A | $7,9 milioni | $8,1 milioni | Sostanzialmente stabili anno su anno. |

| Perdita / utile netto | $(17,6) milioni di perdita netta | $39,1 milioni di utile netto | L’utile dell’anno precedente era distorto dalla rivalutazione non cash dell’earnout liability. |

| Cash, cash equivalents e restricted cash | $48,9 milioni al 31 marzo 2026 | Non direttamente comparabile in questa tabella | Base cash pre-offerta di giugno; la runway aggiornata dopo il finanziamento resta centrale. |

La conclusione finanziaria è lineare. Humacyte ha una storia clinica migliore dopo V012, ma ha ancora bisogno di capitale per commercializzare Symvess, depositare e potenzialmente sostenere l’espansione in emodialisi, finanziare manufacturing, mantenere la pipeline e gestire l’azienda. Finché i ricavi non cresceranno materialmente, il titolo continuerà a portare rischio di diluizione e runway.

Storia commerciale: Symvess è reale, ma ancora iniziale

Symvess è la base dell’identità commercial-stage di Humacyte. L’approvazione FDA nel trauma vascolare ha trasformato la società da piattaforma biotech late-stage a società con un prodotto approvato reale. Questo conta. Molte storie biotech small-cap vivono interamente al futuro. Humacyte può indicare un biologico approvato, vendite iniziali, interesse chirurgico e una piattaforma con molte possibili applicazioni vascolari.

Ma le curve di lancio commerciale nei biologici ospedalieri raramente sono immediate. Symvess non è un farmaco consumer, non è un prodotto da farmacia e non è una pillola semplice che può essere spinta con canali convenzionali. È un condotto vascolare biologico usato in contesti chirurgici seri. L’adozione dipende da formazione dei chirurghi, stocking ospedaliero, workflow dei trauma center, rimborso, training, fiducia clinica ed esperienza istituzionale.

Il dato di vendita del Q1 mostra che l’adozione esiste, ma mostra anche quanto il lancio sia ancora iniziale. Ventinove unità in un trimestre bastano a confermare attività commerciale, non bastano a dimostrare scala. Per questo l’opportunità nell’accesso dialitico conta così tanto. Se ATEV potrà espandersi oltre il trauma in un setting programmato più ampio, la società potrebbe passare da una domanda episodica legata al trauma a un mercato più grande dell’accesso vascolare. Ma quel ponte richiede prima approvazione e poi adozione.

Gli investitori devono ricordare anche la differenza tra uso urgente nel trauma e accesso dialitico. Il trauma è imprevedibile, emergenziale e collegato a capacità ospedaliere specifiche. L’accesso dialitico è un mercato di chronic care infrastructure, con economia, referral pathway e decisioni mediche diverse. La disponibilità off-the-shelf di ATEV può essere preziosa in entrambi i contesti, ma il manuale commerciale non è identico.

La domanda chiave non è se Symvess sia approvato. È se Humacyte riuscirà a trasformare l’approvazione in uso ripetuto, adozione ospedaliera, fiducia nel rimborso e una base di ricavi sufficiente a sostenere la piattaforma senza diluizioni ripetute.

La storia della piattaforma: più di un prodotto, ma non ancora pienamente provata commercialmente

L’appeal di Humacyte è sempre stato più grande di una singola label nel trauma vascolare. La società sviluppa tessuti umani bioingegnerizzati pensati per essere impiantabili universalmente. L’ATEV è l’espressione più avanzata della piattaforma, ma il concetto più ampio include riparazione vascolare, accesso emodialitico, peripheral artery disease, coronary artery bypass grafting, chirurgia cardiaca pediatrica, applicazioni nel diabete di tipo 1 e altri costrutti tissutali.

Questa ambizione di piattaforma è allo stesso tempo il motivo per cui gli investitori seguono la storia e il motivo per cui il profilo di rischio è alto. Se Humacyte riuscirà ad applicare ripetutamente la stessa logica di manufacturing e biologic tissue a più setting clinici, la storia di lungo periodo diventerà molto più grande dei ricavi Symvess nel trauma. Se invece la società incontrerà difficoltà su adozione, cost of goods, scala produttiva, rimborso o espansione regolatoria, la piattaforma potrà restare scientificamente interessante ma finanziariamente difficile.

Il risultato V012 rafforza l’argomento di piattaforma perché aggiunge un altro proof point clinico late-stage. Suggerisce che ATEV possa avere utilità oltre alla riparazione urgente nel trauma, soprattutto in pazienti che affrontano outcome sfavorevoli con approcci standard. I dati si allineano anche alla logica biologica di un vaso off-the-shelf progettato per ridurre problemi di infezione e maturazione legati alle opzioni convenzionali.

Ma il mercato non assegnerà automaticamente pieno valore alla piattaforma. Il valore di piattaforma si guadagna con validazione clinica ripetuta, approvazioni regolatorie, adozione commerciale ed evidenza che l’economia produttiva può funzionare. HUMA oggi ha i primi due elementi parzialmente in campo: un’indicazione trauma approvata e una storia di filing più forte nell’accesso dialitico. Mancano ancora scala commerciale e sostenibilità finanziaria.

Management ed esecuzione

Humacyte è guidata da Laura Niklason, MD, PhD, fondatrice e Chief Executive Officer della società. Il suo background è centrale per l’identità di Humacyte perché questa non è una biotech small-molecule convenzionale. Si trova all’incrocio tra medicina rigenerativa, chirurgia vascolare, manufacturing biologico e tissue engineering. Una piattaforma di questo tipo richiede credibilità scientifica, ma anche disciplina operativa.

La società ha inoltre rafforzato la leadership clinica e commerciale mentre si spinge più a fondo nell’esecuzione del lancio. L’update di maggio 2026 ha evidenziato l’arrivo del Dr. Todd Rasmussen come Chief Surgical Officer, rafforzando la credibilità su educazione chirurgica e trauma/military angle. Questo tipo di leadership conta perché l’adozione dei chirurghi non nasce dalla label da sola. Richiede fiducia clinica, peer education, training ed esposizione istituzionale ripetuta.

Allo stesso tempo, Humacyte ha dovuto ridurre i costi. La riduzione dell’organico e il rinvio delle assunzioni pianificate annunciati a maggio mostrano che la società sta cercando di restringere il focus operativo. In un certo senso è sano: dopo approvazione e dati late-stage, la società deve dare priorità al lavoro commerciale e regolatorio a maggiore valore. Ma la ristrutturazione segnala anche pressione. Le small-cap biotech normalmente non tagliano personale se il capitale è abbondante e i ricavi stanno scalando comodamente.

Da qui in avanti il test del management è molto pratico. Depositare la sBLA nei tempi previsti. Comunicare chiaramente il percorso regolatorio. Evitare promesse eccessive sull’ampiezza della label. Usare in modo efficiente i proventi dell’offerta di giugno. Sostenere il lancio di Symvess senza sovraspendere. Tenere stretto il controllo della qualità produttiva. Mostrare che i ricavi commerciali possono crescere trimestre dopo trimestre. E soprattutto ridurre la paura del mercato che ogni evento clinico positivo venga seguito immediatamente da un’altra grande diluizione.

Ownership, insider activity e SEC filing watch

La pagina SEC filings mostra che Humacyte aveva un nuovo Schedule 13D/A depositato il 15 giugno 2026, oltre a diversi Form 4 del 12 giugno 2026. I Form 4 sembrano includere attività legata ad award azionari per director/officer piuttosto che semplici acquisti insider sul mercato. Un esempio visibile nella lista dei filing è un Form 4 per Emery N. Brown che mostra un award di 80.000 stock option con strike price di 1,08 dollari e vesting schedule a partire da un anno dopo.

Questo conta perché i trader retail spesso trattano ogni filing insider come automaticamente bullish o bearish. È troppo grossolano. Option awards, equity compensation e grant ordinari non sono la stessa cosa di acquisti insider open market. Possono allineare il management agli azionisti nel tempo, ma non hanno lo stesso segnale di un executive che usa capitale personale per comprare azioni sul mercato.

Il Schedule 13D/A del 15 giugno merita monitoraggio perché gli amendment sulla beneficial ownership possono fornire informazioni su holder significativi, variazioni di ownership o accordi correlati. Tuttavia, i filing di ownership vanno interpretati direttamente dal documento depositato, non da sintesi social. Per un contenuto pubblico, la formulazione pulita è che un nuovo 13D/A è comparso nella pagina SEC della società il 15 giugno, mentre i dettagli di ownership devono essere verificati direttamente nel filing prima di fare affermazioni più forti.

La distinzione importante è tra acquisti/vendite effettivi e filing di equity compensation. L’attività Form 4 del 12 giugno visibile nella lista non dovrebbe essere descritta come accumulo insider generalizzato se non vengono confermate transazioni di acquisto diretto nei filing.

Sentiment retail e psicologia di trading

HUMA è esattamente il tipo di small-cap biotech capace di generare sentiment retail contrastante. Il lato bullish vede un prodotto approvato dalla FDA, una vera piattaforma di medicina rigenerativa, un forte readout Phase 3 V012, una possibile sBLA nella seconda metà del 2026, rilevanza trauma/military e un mercato potenzialmente più ampio nell’accesso dialitico. Il lato bearish vede ricavi attuali bassi, una struttura di costi elevata, diluizione ripetuta, un titolo che tratta vicino alla psicologia del prezzo di offering e il rischio che la promessa clinica non si trasformi rapidamente in scala commerciale.

Riconoscere questa frattura è utile perché spiega il tape. Un catalyst biotech pulito spesso produce una reazione semplice: buoni dati, stock su; dati cattivi, stock giù. HUMA è più complicata. I dati sono stati buoni, ma l’offerta ha assorbito il momentum. Questo crea frustrazione tra i retail holder, soprattutto tra chi si aspettava un movimento post-data lineare. Crea anche opportunità per trader di breve specializzati in setup post-offering, ma quella è struttura di trading, non conclusione fondamentale.

Su piattaforme come Stocktwits, Reddit e X, il dibattito probabilmente non riguarda più se V012 fosse positivo. Il dibattito è se la diluizione fosse già prezzata, se l’offerta a 1,05 dollari crei un floor o un anchor, se l’investor event possa resettare il sentiment e se la timeline sBLA sia abbastanza vicina da mantenere interesse. Questo tipo di sentiment può muovere una small-cap, ma va trattato come psicologia dei trader, non come conferma fattuale.

La lettura bilanciata più forte è che HUMA oggi ha più credibilità clinica ma deve ancora ricostruire fiducia con il mercato. Gli investitori potrebbero premiare il titolo se il management fornirà una guida chiara sul filing, mostrerà uso disciplinato dei proventi e dimostrerà crescita dei ricavi Symvess. Potrebbero invece punirlo se i ricavi resteranno lenti, se l’overhang dell’offerta persisterà, se l’opzione underwriter aggiungerà pressione o se il percorso sBLA risulterà meno chiaro di quanto oggi la società preveda.

Bull Case

Il bull case parte dai dati. V012 non ha prodotto soltanto un segnale vago. Ha raggiunto l’endpoint primario con un vantaggio chiaro nei catheter-free days e l’update del 15 giugno ha aggiunto endpoint secondari e dettagli su infezioni/safety. In una popolazione ad alto unmet need, questo dà a Humacyte un argomento più forte secondo cui ATEV può risolvere un problema clinico reale.

Il secondo punto bullish è regolatorio. Humacyte ha già ottenuto l’approvazione FDA per Symvess nel trauma vascolare degli arti, quindi la società ha già tagliato una volta il traguardo FDA con la piattaforma ATEV. Non garantisce approvazione nell’accesso dialitico, ma offre esperienza regolatoria, precedente produttivo e identità commercial-stage che molti peer biotech small-cap non hanno.

Il terzo punto bullish è l’opzionalità. Se ATEV funziona nel trauma e mostra dati convincenti nell’accesso dialitico, gli investitori potrebbero iniziare ad assegnare valore a una piattaforma vascolare più ampia. Peripheral artery disease, coronary artery bypass grafting e altre applicazioni tissutali restano future-facing, ma una seconda indicazione approvata o approvabile renderebbe la tesi di piattaforma più difficile da liquidare.

Il quarto punto bullish è che il finanziamento, pur diluitivo, può dare a Humacyte più spazio per eseguire. Se l’offerta da 50 milioni allunga la runway abbastanza da depositare la sBLA, sostenere le attività di lancio e ridurre la pressione immediata sulla continuità aziendale, l’aumento potrebbe essere visto come doloroso ma necessario. Nel biotech, la diluizione dopo buoni dati non è automaticamente fatale se finanzia esecuzione che crea valore.

Scenario Bull

V012 supporta un deposito tempestivo della supplemental BLA nella seconda metà del 2026; la FDA accetta la domanda senza ritardi importanti; la label target resta commercialmente significativa; le vendite Symvess continuano a crescere; il finanziamento di giugno riduce la pressione di bilancio nel breve; e il mercato inizia a valutare Humacyte come piattaforma vascolare multi-indicazione invece che come semplice lancio trauma single-product.

Bear Case e red flags

Il bear case parte dalla diluizione. Humacyte ha prezzato 47,6 milioni di nuove azioni a 1,05 dollari subito dopo il catalyst V012. È un’emissione grande rispetto al conteggio azionario esistente. Anche se i dati clinici sono forti, il mercato può continuare ad ancorarsi al prezzo di offerta finché non vedrà evidenza che il nuovo capitale basti e che ulteriori aumenti non siano imminenti.

Il secondo punto bearish è la scala commerciale. Le vendite Symvess sono reali ma iniziali. Ventinove unità e 0,5 milioni di dollari di ricavi prodotto nel Q1 non bastano a sostenere le ambizioni attuali della società. Se l’adozione ospedaliera resterà lenta, Humacyte potrebbe continuare a dipendere da capitale esterno anche dopo milestone clinici positivi.

Il terzo punto bearish è il rischio regolatorio. Un risultato interim Phase 3 positivo supporta un filing, ma la FDA può comunque sollevare domande. Ampiezza della label, safety, manufacturing, selezione pazienti, completezza del dataset e possibili impegni post-approval possono influenzare tempistica e valore commerciale. Un filing nella seconda metà del 2026 è un piano, non un’approvazione.

Il quarto punto bearish è l’economia produttiva. Il dettaglio COGS del Q1 2026 includeva riserva inventariale e costi da capacità produttiva inutilizzata. Se la società non riuscirà a migliorare l’efficienza del manufacturing con la crescita dei volumi, gross margin e cash burn potrebbero restare problematici. Le piattaforme di medicina rigenerativa possono essere potenti, ma possono anche essere costose da scalare.

Il quinto punto bearish è la fiducia del mercato. Gli holder HUMA hanno appena visto uno schema familiare nelle small-cap biotech: buoni dati seguiti rapidamente da diluizione. Questo può creare un overhang persistente. La società dovrà mostrare che il progresso clinico futuro si traduce in creazione di valore per gli azionisti, non soltanto in nuovi round di finanziamento.

Scenario Bear

L’overhang dell’offerta persiste, le vendite Symvess restano troppo piccole per cambiare la storia finanziaria, il deposito sBLA slitta o riceve una review FDA più complessa del previsto, i costi produttivi restano pesanti e il mercato continua a scontare la piattaforma perché ogni milestone positivo sembra richiedere altra equity financing.

Base Case

Il base case sta nel mezzo tra l’entusiasmo per i dati V012 e la realtà dura dell’offerta. Humacyte probabilmente ha oggi una storia più forte rispetto a prima del 10 giugno. I dati V012 sono clinicamente significativi, il dettaglio del 15 giugno migliora la qualità della narrativa e il deposito sBLA pianificato offre agli investitori un milestone chiaro. Allo stesso tempo, la società resta finanziariamente fragile, commercialmente iniziale e molto dipendente dall’esecuzione.

Nel base case, HUMA resta una biotech catalyst-driven con asset clinici reali ma alto rischio azionario. Il titolo può muoversi su commenti dell’investor event, assorbimento dell’offerta, news sull’opzione underwriter, timing del filing sBLA, aggiornamenti sulle vendite Symvess e qualunque feedback FDA. Non è ancora una storia biotech commerciale matura. È una storia di transizione: da promessa di piattaforma a esecuzione di lancio ed espansione di label.

Scenario Base

Humacyte deposita la supplemental BLA nella seconda metà del 2026, ma il mercato aspetta accettazione FDA, timeline di review più chiara e ricavi commerciali più forti prima di assegnare una valutazione molto più alta. Il titolo resta volatile, con credibilità clinica migliorata ma diluizione e runway ancora centrali.

Cosa ridurrebbe davvero il rischio HUMA da qui?

Il primo evento di de-risking sarebbe un deposito pulito della supplemental BLA. Depositare nei tempi previsti confermerebbe che Humacyte può convertire V012 in un pacchetto regolatorio. Il secondo evento sarebbe l’accettazione FDA e una timeline di review chiara. L’accettazione non significa approvazione, ma sposterebbe la storia dalla guidance aziendale al processo FDA.

Il terzo evento di de-risking sarebbe una crescita più forte dei ricavi Symvess. Gli investitori non hanno bisogno di vedere piena maturità commerciale subito, ma hanno bisogno di vedere progressi sequenziali che suggeriscano adozione ospedaliera più ripetibile. Un prodotto che cresce da cinque a 29 unità è interessante. Un prodotto che continua ad espandersi trimestre dopo trimestre diventa più investibile.

Il quarto evento sarebbe maggiore chiarezza sulla runway dopo l’aumento di giugno. La società deve mostrare che il finanziamento crea un ponte operativo significativo e non solo sollievo temporaneo. La guidance aggiornata sulla runway conta perché la precedente posizione cash e il linguaggio di going concern tenevano il rischio finanziario al centro della storia.

Il quinto evento sarebbe il miglioramento dell’economia produttiva. La piattaforma Humacyte è investibile solo quanto lo è la sua capacità di produrre, distribuire e supportare ATEV economicamente. Migliore utilization, minore cost of goods ed evidenza che i process improvements funzionano aiuterebbero il mercato a credere che la piattaforma possa scalare.

Merlintrader Bottom Line

L’update del 15 giugno di Humacyte rende la storia V012 più credibile, non meno. La società ha ora un dataset più completo che mostra un chiaro vantaggio nei giorni senza catetere, endpoint secondari di supporto, tassi di infezione riportati più bassi e un percorso previsto verso supplemental BLA per adulti con end-stage kidney disease ad aumentato rischio di fallimento della maturazione di AV fistula. È un vero milestone clinico.

Ma HUMA non è una storia pulita del tipo “buoni dati uguale facile upside”. L’offerta da 50 milioni di dollari ha cambiato il tape di breve periodo e la base di ricavi attuale resta piccola. Symvess è approvato, ma ancora iniziale. ATEV ha potenziale di piattaforma, ma il potenziale deve essere convertito in filing, approvazioni, ricavi e cash burn gestibile. I dati di giugno 2026 hanno migliorato il lato clinico dell’equazione; il mercato aspetta ancora che il lato finanziario recuperi.

La cornice corretta è quindi equilibrata. HUMA è passata da “in attesa di V012” a “dimostrare che V012 può diventare un filing FDA, un’espansione di label e una vera opportunità commerciale”. I prossimi mesi riguardano l’esecuzione. Se Humacyte depositerà la sBLA nei tempi, manterrà una comunicazione regolatoria pulita, farà crescere i ricavi Symvess e userà bene il finanziamento di giugno, la vittoria V012 potrà diventare il secondo grande pilastro della piattaforma ATEV. In caso contrario, il mercato potrebbe continuare a trattare HUMA come una small-cap biotech scientificamente interessante ma finanziariamente sotto pressione.

Per trader e lettori, la chiave è separare tre livelli: il risultato clinico è stato positivo; il finanziamento è stato diluitivo; il dibattito d’investimento ora dipende dalla capacità della società di trasformare il risultato clinico in valore regolatorio e commerciale prima che le preoccupazioni sulla struttura del capitale tornino in primo piano.

Fonti primarie e riferimenti

- Humacyte — comunicato del 15 giugno 2026 con update dettagliato della presentazione V012

- Humacyte — comunicato del 10 giugno 2026 sui risultati top-line interim Phase 3 V012

- Humacyte — risultati finanziari Q1 2026 e business update del 13 maggio 2026

- Humacyte — pagina SEC filings

- Merlintrader Europe — archivio blog

- Merlintrader Free Biotech Catalyst Calendar

Humacyte (Nasdaq: $HUMA): V012 Presentation Adds Depth to the Dialysis Access Story, but Dilution and Execution Still Define the Next Test

Humacyte’s June 2026 story has moved beyond the initial V012 headline. The company has now released and presented a fuller Phase 3 picture in female dialysis access patients, including secondary efficacy endpoints, infection data, safety detail and the planned supplemental BLA path. The clinical update is stronger than a simple top-line press release, but the stock story remains complicated by the freshly priced $50 million equity offering, early Symvess commercialization, low current revenue and a balance sheet that still needs careful management.

Next Watch Items After the June 15 Update

The V012 catalyst is no longer pending. The top-line data were announced on June 10, 2026, and the more detailed presentation update was released on June 15 after the Society for Vascular Surgery’s Vascular Annual Meeting. The next watch items are now the investor event scheduled for June 15 at 5:00 p.m. ET, any additional management commentary on the supplemental BLA package, final details around the June equity raise and underwriter option, updated cash runway after the financing, and the company’s planned supplemental BLA filing in the second half of 2026.

Executive Summary

Humacyte is no longer a simple “data event” story. The company has crossed the June V012 catalyst, reported a statistically significant Phase 3 interim win, presented more complete data at SVS VAM, and added enough secondary and safety context to make the dialysis access story more substantial. But the market also received a very clear reminder that clinical progress does not eliminate financing risk in small-cap biotech. The $50 million common-stock offering priced at $1.05 per share sits directly beside the clinical win, and that combination defines the current HUMA tape.

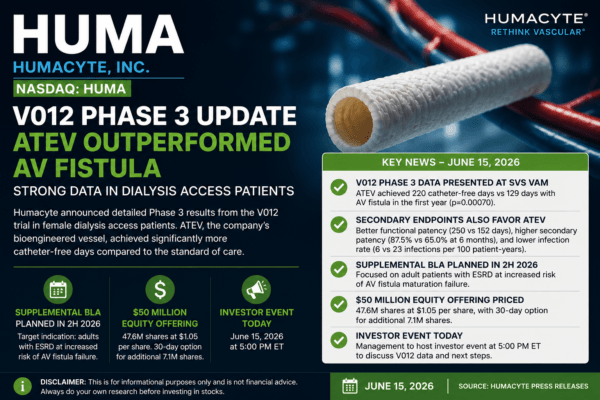

The most important clinical point remains straightforward. In the V012 Phase 3 study, women who received Humacyte’s acellular tissue engineered vessel, or ATEV, averaged 220 catheter-free days over the first year, compared with 129 catheter-free days for women who received autologous AV fistula, the current standard of care. That is a 91-day average advantage, and Humacyte reported statistical significance with p=0.00070. In a hemodialysis access setting where catheter dependence can mean infection risk, complications and repeated intervention burden, that is an intuitive endpoint for investors and clinicians to understand.

The June 15 update matters because it adds detail beyond the headline. Humacyte disclosed additional secondary efficacy measures: six-month catheter-free days averaged 88 days for ATEV versus 32 days for AV fistula; functional patency over 12 months averaged 250 days for ATEV versus 152 days for AV fistula; six-month secondary patency was 87.5% for ATEV versus 65.0% for AV fistula; and twelve-month secondary patency was 77.5% for ATEV versus 62.5% for AV fistula, although the twelve-month secondary patency comparison was reported with p=0.16 and therefore should not be framed as statistically significant.

Safety detail also became more useful. Humacyte reported infections at about six infections per 100 patient-years in the ATEV group versus 23 infections per 100 patient-years in the AV fistula group. The company also said no infections in the ATEV group were tied to the study access itself, compared with three such infections in the AV fistula group, and no ruptures occurred in either group. Serious adverse events were reported at 1.73 for ATEV versus 4.77 for AV fistula on an adjusted patient-years basis. Adverse events of special interest were 2.71 for ATEV versus 3.88 for AV fistula; thrombotic events were 0.75 for ATEV versus 0.51 for AV fistula, with 75.0% of ATEV thrombosis cases successfully resolved compared with 37.5% for AV fistula; and stenotic events were 1.62 for ATEV versus 2.29 for AV fistula.

The regulatory path is now more visible, but not complete. Humacyte plans to file a supplemental Biologics License Application with the FDA during the second half of 2026. The currently planned target indication is focused on adult patients with end-stage kidney disease who are at increased risk of AV fistula maturation failure. That target framing is important because it suggests Humacyte is not simply trying to win a broad “dialysis access” label in the abstract; it is trying to position ATEV where standard fistula formation is more likely to fail or produce prolonged catheter dependence.

The financial story is the counterweight. Humacyte’s Q1 2026 commercial sales of Symvess were $0.5 million, or 29 units, compared with $0.1 million and five units in Q1 2025. That is progress, but still a very small revenue base relative to the company’s R&D, manufacturing, commercial and regulatory ambitions. Q1 2026 R&D expense was $19.5 million, G&A expense was $7.9 million, and net loss was $17.6 million. Cash, cash equivalents and restricted cash were $48.9 million as of March 31, 2026, before the latest June offering proceeds.

The clean read is this: HUMA now has a stronger clinical and regulatory story than it had before the V012 readout, but the equity story is still not clean. The stock has to absorb dilution, prove commercial execution, file and move through the supplemental BLA process, and show that Symvess and ATEV can become more than a compelling scientific platform. Good clinical data bought Humacyte credibility. It did not buy the company a free pass.

What Changed With the June 15, 2026 Update

The June 10 release gave investors the top-line V012 result. The June 15 update gives the market the fuller presentation framing. That difference matters. In biotech, a headline p-value can move a stock for a few hours, but a more complete dataset decides whether the story can survive beyond the first trading reaction. For Humacyte, the June 15 update strengthens the clinical narrative because it shows that the advantage was not limited to one isolated number.

The primary endpoint was already known: ATEV outperformed AV fistula on catheter-free days in the prespecified interim analysis of the first 80 patients who had completed 12 months of follow-up. The June 15 presentation update reinforces that result and then layers on additional endpoints that matter clinically. A product designed to replace or supplement standard access options in hemodialysis does not need only one positive number. It needs a pattern that makes sense across catheter avoidance, patency, infections, access-related complications and durability.

Humacyte’s new update points in that direction, with one important caveat: investors should not treat every number equally. The six-month catheter-free-days endpoint, twelve-month functional patency and six-month secondary patency all showed strong reported p-values in favor of ATEV. The twelve-month secondary patency figure numerically favored ATEV but was reported with p=0.16, which means it should be described as a numerical advantage rather than a statistically significant one. That distinction is important for credibility, especially in a report intended for serious biotech readers.

| V012 Measure | ATEV | AV Fistula | Reported p-value | Merlintrader Read-Through |

|---|---|---|---|---|

| Average catheter-free days over first year | 220 days | 129 days | p=0.00070 | Primary endpoint met; clinically intuitive 91-day average advantage. |

| Six-month catheter-free days | 88 days | 32 days | p=0.00009 | Supports earlier catheter-avoidance benefit. |

| Functional patency over 12 months | 250 days | 152 days | p=0.00057 | Important because access durability matters commercially and clinically. |

| Six-month secondary patency | 87.5% | 65.0% | p=0.0013 | Favorable near-term patency signal. |

| Twelve-month secondary patency | 77.5% | 62.5% | p=0.16 | Numerically favorable, but not statistically significant based on the reported p-value. |

The most useful way to frame the update is not “HUMA announced the same data again.” That would miss the point. The better framing is that Humacyte now has a more complete clinical argument for its supplemental BLA package. The June 10 top-line result established that V012 met the primary endpoint. The June 15 release gives the market more detail on how broad that result appears across key dialysis-access measures. That matters because FDA review, physician adoption and payer discussions are rarely driven by a single metric in isolation.

HUMA should no longer be framed as “heading into the June 11 V012 catalyst.” The catalyst has already occurred. The story is now post-readout and post-presentation. The next phase is about supplemental BLA execution, FDA review risk, label framing, commercial translation and the balance sheet after the $50 million financing.

The V012 Result in Plain English

Hemodialysis patients need reliable access to the bloodstream. The access must allow blood to leave the body, pass through a dialysis machine, and return safely. The standard approach is often an autologous arteriovenous fistula, where a surgeon connects an artery and a vein. In theory, fistulas are durable and preferred. In practice, they can take time to mature, may fail to mature, and can force patients to remain dependent on catheters.

Catheters are clinically problematic because they can be associated with bloodstream infections and other complications. The longer a patient remains catheter-dependent, the more time that patient spends exposed to catheter-related risk. That is why catheter-free days are not an abstract endpoint. They are easy to understand: more catheter-free days means less time relying on a catheter.

Humacyte’s ATEV is designed as an off-the-shelf bioengineered human vessel. The idea is to provide a vascular conduit that surgeons can use when the patient needs access and when conventional options may not work well enough. The product is not a synthetic graft in the simple commodity sense; it is derived from cultured human cells, then processed into an acellular vessel intended to be universally implantable. The platform goal is to combine device-like availability with biologic integration characteristics.

In V012, the primary comparison was between ATEV and AV fistula in female dialysis access patients. The female-patient focus is important. Humacyte has repeatedly emphasized that women can face worse fistula-maturation challenges than men, including vessel-size and anatomy issues. The trial’s target population therefore has a clear clinical rationale: if standard fistula access fails more often or matures less reliably in certain patients, an off-the-shelf alternative may have a more defensible role.

The reported result is clinically clean enough for a broad market audience. ATEV patients averaged 220 catheter-free days versus 129 days for AV fistula patients in the first year. That 91-day average advantage is the core of the story. It is large, intuitive and statistically significant. The secondary endpoints released on June 15 make the story more durable because they add functional-patency and secondary-patency context rather than leaving investors with one number and a press-release headline.

Still, the V012 result should not be confused with approval. A positive Phase 3 interim analysis and a strong presentation update support the planned filing. They do not guarantee FDA acceptance, priority review, approval, final label language, payer coverage, physician adoption or commercial success. The FDA still has to review the complete package, including efficacy, safety, study conduct, manufacturing, labeling, benefit-risk, post-marketing commitments if any, and how the V012 data fit with earlier AV-access data such as V007.

Why the Female Dialysis Access Population Matters

One reason the V012 data are more interesting than a generic vascular-access trial is the population. Female dialysis patients are not a random subgroup chosen for marketing effect. They represent a high-unmet-need group in which fistula maturation and catheter dependence can be especially challenging. Humacyte’s own framing is that women receiving AV access face clear unmet needs because fistulas often fail to develop properly, forcing too many patients to rely on catheters.

For investors, this has two implications. The positive implication is that a more focused high-risk population can make the clinical and regulatory argument easier to understand. Instead of saying “ATEV should replace fistulas everywhere,” Humacyte can argue that ATEV may be particularly useful in adults with end-stage kidney disease who are at increased risk of AV fistula maturation failure. That is a more targeted and potentially more defensible indication.

The more cautious implication is that a targeted indication also requires careful market-size interpretation. A smaller, more defined label can support adoption in a high-need niche, but it does not automatically mean that the entire hemodialysis access market becomes available immediately. The commercial opportunity will depend on final label language, clinical guidelines, physician comfort, reimbursement, hospital purchasing behavior, manufacturing capacity and real-world performance.

This distinction matters because HUMA has often traded like a broad platform story. The platform narrative is powerful: trauma, dialysis access, peripheral artery disease, coronary artery bypass grafting, pediatric heart surgery, type 1 diabetes and other tissue applications. But public-market value creation will likely depend first on execution in concrete indications. Vascular trauma gave Humacyte its first FDA-approved product. V012 may support a second major indication. The company still has to turn those milestones into revenue and adoption.

The Regulatory Setup After V012

Humacyte already has an FDA-approved ATEV product for vascular trauma. Symvess is indicated for adults as a vascular conduit for extremity arterial injury when urgent revascularization is needed to avoid imminent limb loss and autologous vein graft is not feasible. That approval is important because Humacyte is not a purely pre-commercial biotech anymore. It has an approved biologic product and a live commercial launch.

The hemodialysis access indication is separate. Humacyte has been clear that, outside the approved extremity vascular trauma indication, ATEV remains investigational and has not been approved for sale by the FDA or any other regulatory agency. This point must remain visible in any public-facing report because the V012 data are supportive, not equivalent to a commercial label expansion.

The company now plans to file a supplemental BLA with the FDA during the second half of 2026. The target indication currently planned is adult patients with end-stage kidney disease who are at increased risk of AV fistula maturation failure. If the filing is submitted, the next sequence would include FDA acceptance review, assignment of a review timeline, possible information requests, label discussions, manufacturing review and an eventual regulatory decision.

The key question is how the FDA will view the totality of evidence. V012 gives Humacyte a strong interim dataset in female dialysis access patients. Earlier V007 data also remain relevant because Humacyte has previously positioned AV access as a broader late-stage program. The regulatory package will need to show that the benefit-risk balance is favorable for the proposed population, not only that one endpoint was positive.

The V012 update improves the probability that Humacyte can submit a more persuasive supplemental BLA package. It does not remove FDA review risk. The market should separate “the company has a stronger filing story” from “the indication is already approved.”

| Timing | Event | Status | Why It Matters |

|---|---|---|---|

| December 2024 | FDA approval of Symvess in extremity vascular trauma | Completed | Establishes Humacyte as a commercial-stage biotech with an approved ATEV product. |

| June 10, 2026 | Top-line V012 Phase 3 interim result | Completed | ATEV met the primary endpoint versus AV fistula on catheter-free days. |

| June 15, 2026 | Detailed V012 presentation update | Completed | Adds secondary endpoint and safety context after SVS VAM presentation. |

| June 15, 2026 at 5:00 p.m. ET | Investor event on V012 | Scheduled | May provide additional management framing on filing strategy, patient selection and commercial implications. |

| Second half 2026 | Planned supplemental BLA filing | Pending | Next major regulatory execution milestone for the AV access indication. |

The Offering: Why the Stock Setup Is Still Not Clean

The most important non-clinical event in the HUMA story is the June 2026 financing. On the same day Humacyte announced the positive V012 result, it also announced a public offering. The company later priced the offering at 47,619,048 shares of common stock at $1.05 per share, for expected gross proceeds of $50 million before underwriting discounts, commissions and other offering expenses. The underwriters also received a 30-day option to purchase up to 7,142,857 additional shares at the public offering price, less underwriting discounts and commissions.

This is why the stock reaction cannot be analyzed only through the clinical lens. From a scientific and regulatory perspective, V012 was positive. From a capital-markets perspective, shareholders immediately had to absorb a large common-stock issuance. In small-cap biotech, that combination is common: companies often raise into strength because the catalyst creates liquidity and because clinical success usually increases the need to fund the next stage. But for existing shareholders, the math still matters.

The previous Merlintrader update framed the base offering as adding 47,619,048 new shares. Using the 222,019,108 common shares outstanding as of the April 23, 2026 record date disclosed in the company’s June 9 8-K, that base issuance equals roughly 21.45% of that record-date share count and about 17.66% of the simple pro forma common share total after issuance. If the underwriter option is fully exercised, total new shares would rise to 54,761,905, equal to about 24.67% of the record-date share count and about 19.79% of the simple pro forma total.

That is not a fully diluted capitalization model. It does not include options, warrants, RSUs, future ATM sales, future equity programs, convertibles or additional financing. But it is enough to show why the offering matters. The market is not deciding only whether V012 was clinically good. It is deciding whether the clinical improvement justifies the new share count and whether the proceeds give Humacyte enough runway to execute the sBLA and commercial plan without immediately returning to the market.

| Financing Scenario | New Shares | Gross Proceeds | Simple Dilution Frame |

|---|---|---|---|

| Base public offering | 47,619,048 shares | $50.0 million before underwriting discounts, commissions and expenses | About 21.45% of the April 23 record-date common shares; about 17.66% of the simple pro forma common total. |

| If underwriter option is fully exercised | 54,761,905 total new shares | About $57.5 million gross before underwriting discounts, commissions and expenses | About 24.67% of the April 23 record-date common shares; about 19.79% of the simple pro forma common total. |

| Use of proceeds | Not applicable | Net proceeds to company after expenses | Commercialization of Symvess, planned hemodialysis BLA supplement filing, pipeline candidates, working capital and general corporate purposes. |

The offering does not erase the V012 win, but it changes the stock setup. The near-term HUMA tape is a tug-of-war between a stronger clinical story and a larger share-count/dilution burden. That is exactly why the next investor-event commentary and updated runway assumptions matter.

Financial Position, Symvess Revenue and Runway Pressure

Humacyte’s Q1 2026 numbers explain why the company raised capital immediately after the V012 catalyst. Symvess commercial sales increased, but they remain small. The company reported commercial sales of Symvess of $0.5 million, or 29 units, in Q1 2026, compared with $0.1 million, or five units, in Q1 2025. Product adoption is moving in the right direction, but the revenue base is still tiny relative to the operating cost structure.

Total revenue was $495,000 in Q1 2026, compared with $517,000 in Q1 2025. That headline comparison looks flat to slightly lower, but the mix changed. Product revenue improved, while contract revenue from a research collaboration declined because the relevant phase of the collaboration had been completed. This is a meaningful distinction. The business is becoming more product-driven, but it has not yet reached commercial scale.

Cost of goods sold was $2.0 million in Q1 2026, compared with $0.1 million in Q1 2025. Humacyte said only $0.2 million of Q1 2026 COGS related to units recorded as sales revenue, while the remainder was primarily a $1.6 million inventory reserve and overhead tied to unused production capacity. That is an important signal for investors: manufacturing scale and utilization matter. If Symvess and future ATEV indications grow, operating leverage could improve. If revenue remains slow, unused capacity and inventory economics can weigh heavily.

R&D expense was $19.5 million in Q1 2026, up from $15.4 million in Q1 2025. Humacyte attributed the increase largely to material costs, mainly from non-commercial manufacturing runs associated with CTEV and process improvement work designed to reduce cost of goods sold over time. G&A expense was $7.9 million, broadly consistent with $8.1 million in the prior-year quarter. Net loss was $17.6 million, compared with net income of $39.1 million in Q1 2025, but the prior-year comparison was heavily affected by non-cash income from contingent earnout liability remeasurement.

Cash, cash equivalents and restricted cash were $48.9 million as of March 31, 2026. Humacyte also announced workforce and operating cost reductions in May 2026, including a reduction of approximately 45 employees and deferral of planned hires. The company estimated net savings of approximately $14.3 million during the remainder of 2026, after severance and related costs. That cost discipline matters, but the June raise shows it was not enough by itself to remove financing risk.

| Metric | Q1 2026 | Q1 2025 | Read-Through |

|---|---|---|---|

| Symvess commercial sales | $0.5 million / 29 units | $0.1 million / 5 units | Clear product growth from a very small base. |

| Total revenue | $495,000 | $517,000 | Flat headline revenue because product growth was offset by lower contract revenue. |

| Cost of goods sold | $2.0 million | $0.1 million | Includes inventory reserve and underutilized production capacity costs. |

| R&D expense | $19.5 million | $15.4 million | Higher spending tied partly to non-commercial manufacturing and process improvement work. |

| G&A expense | $7.9 million | $8.1 million | Broadly stable year over year. |

| Net loss / income | $(17.6) million net loss | $39.1 million net income | Prior-year income was distorted by non-cash earnout liability remeasurement. |

| Cash, cash equivalents and restricted cash | $48.9 million at March 31, 2026 | Not directly comparable in this table | Pre-June-offering cash base; updated runway after financing remains a key watch item. |

The financial conclusion is straightforward. Humacyte has a better clinical story after V012, but it still needs capital to commercialize Symvess, file and potentially support the hemodialysis expansion, fund manufacturing, maintain pipeline work and run the company. Until revenue ramps materially, the stock will continue to carry dilution and runway risk.

Commercial Story: Symvess Is Real, but Still Early

Symvess is the foundation of Humacyte’s commercial-stage identity. FDA approval in vascular trauma changed the company’s status from late-stage platform biotech to a company with a real approved product. That matters. Many small-cap biotech stories live entirely in future-tense language. Humacyte can point to an approved biologic, initial sales, surgeon interest and a platform with multiple possible vascular applications.

But commercial launch curves in hospital-based biologics are rarely instant. Symvess is not a consumer drug, not a pharmacy product and not a simple pill that can be marketed broadly through conventional channels. It is a biologic vascular conduit used in serious surgical contexts. Adoption depends on surgeon education, hospital stocking, trauma-center workflows, reimbursement, training, clinical confidence and institutional experience.

The Q1 sales figure shows that adoption exists, but it also shows how early the launch remains. Twenty-nine units in a quarter is enough to confirm commercial activity, not enough to prove scale. That is why the dialysis-access opportunity matters so much. If ATEV can expand beyond trauma into a larger planned-use setting, the company could move from episodic trauma demand toward a broader vascular-access market. But that bridge requires approval first and adoption second.

Investors should also remember the difference between urgency-driven trauma use and dialysis access. Trauma use can be unpredictable, emergent and tied to specific hospital capabilities. Dialysis access is a chronic-care infrastructure market with different economics, referral pathways and physician decision-making. ATEV’s off-the-shelf availability could be valuable in both settings, but the commercial playbook is not identical.

The key question is not whether Symvess is approved. It is whether Humacyte can turn approval into repeat usage, hospital adoption, reimbursement confidence and a revenue base large enough to support the platform without repeated equity dilution.

The Platform Story: More Than One Product, but Not Yet Fully Proven Commercially

Humacyte’s appeal has always been larger than one vascular-trauma label. The company is developing bioengineered human tissues intended to be universally implantable. The ATEV is the most advanced expression of that platform, but the broader concept includes vascular repair, hemodialysis access, peripheral artery disease, coronary artery bypass grafting, pediatric heart surgery, type 1 diabetes applications and other tissue constructs.

That platform ambition is both the reason investors pay attention and the reason the risk profile is high. If Humacyte can repeatedly apply the same manufacturing and biologic-tissue logic across multiple clinical settings, the long-term story becomes much bigger than Symvess trauma revenue. If the company struggles with adoption, cost of goods, manufacturing scale, reimbursement or regulatory expansion, the platform story may remain scientifically interesting but financially difficult.

The V012 result strengthens the platform argument because it adds another late-stage clinical proof point. It suggests that ATEV may have utility beyond urgent trauma repair, especially in patients who face poor outcomes with standard access approaches. The data also align with the biological logic of an off-the-shelf vessel designed to avoid infection and maturation problems associated with conventional access options.

But the market will not give full platform value automatically. Platform value is earned through repeated clinical validation, regulatory approvals, commercial uptake and evidence that manufacturing economics can work. HUMA now has the first two pieces partly in place: one approved trauma indication and a stronger filing case for dialysis access. The missing pieces are still commercial scale and financial durability.

Management and Execution

Humacyte is led by Laura Niklason, MD, PhD, the company’s founder and Chief Executive Officer. Her background is central to the company’s identity because Humacyte is not a conventional small-molecule biotech. It sits at the intersection of regenerative medicine, vascular surgery, biologics manufacturing and tissue engineering. That kind of platform requires scientific credibility, but also operational discipline.

The company has also been adding clinical and commercial leadership as it moves deeper into launch execution. The May 2026 update highlighted the addition of Dr. Todd Rasmussen as Chief Surgical Officer, strengthening the surgical-education and trauma/military credibility angle. That type of leadership matters because surgeon adoption is not created by a label alone. It requires clinical trust, peer education, training and repeated institutional exposure.

At the same time, Humacyte has had to reduce costs. The workforce reduction and planned-hire deferrals announced in May show that the company is trying to narrow its operating focus. That is healthy in one sense: after approval and late-stage data, the company needs to prioritize the highest-value commercial and regulatory work. But restructuring also signals pressure. Small-cap biotech companies usually do not cut headcount if capital is abundant and revenue is scaling comfortably.

The management test from here is therefore very practical. File the sBLA on schedule. Communicate the regulatory path clearly. Avoid overpromising on label breadth. Use the June offering proceeds efficiently. Support Symvess launch without overspending. Keep manufacturing quality tight. Show that commercial revenue can grow quarter by quarter. And, above all, reduce the market’s fear that every positive clinical event will be followed immediately by another large dilutive financing.

Ownership, Insider Activity and SEC Filing Watch

The SEC filing page shows that Humacyte had a new Schedule 13D/A filed on June 15, 2026, as well as multiple Form 4 filings on June 12, 2026. The Form 4 filings appear to include director/officer equity-award activity rather than simple open-market insider purchases. One example visible in the filing list is a Form 4 for Emery N. Brown showing an 80,000 stock option award with an exercise price of $1.08 and a vesting schedule beginning one year later.

This matters because retail traders often treat any insider filing as automatically bullish or bearish. That is too crude. Option awards, equity compensation and routine grants are not the same as open-market insider buying. They may align management with shareholders over time, but they do not carry the same signal as an executive using personal cash to buy shares in the open market.

The June 15 Schedule 13D/A deserves monitoring because beneficial-ownership amendments can provide information about significant holders, ownership changes or related arrangements. However, ownership filings should be interpreted directly from the filed document, not from social-media summaries. For publication purposes, the clean statement is that a new 13D/A appeared on the company’s SEC filing page on June 15, while the underlying ownership details should be checked directly in the filing before making any stronger claim.

The important distinction is between actual buying/selling and equity-compensation filings. The June 12 Form 4 activity visible in the filing list should not be described as broad insider accumulation unless direct purchase transactions are confirmed in the filings.

Retail Sentiment and Trading Psychology

HUMA is exactly the kind of small-cap biotech that can produce conflicting retail sentiment. The bullish side sees an FDA-approved product, a real regenerative-medicine platform, a strong V012 Phase 3 readout, possible sBLA filing in the second half of 2026, military/trauma relevance and a potentially larger dialysis-access market. The bearish side sees low current revenue, a high cost base, repeated dilution, a stock trading near offering psychology and the risk that clinical promise does not translate quickly into commercial scale.

This split is healthy to acknowledge because it explains the tape. A clean biotech catalyst often produces a simple reaction: good data, stock up; bad data, stock down. HUMA is more complicated. The data were good, but the offering absorbed the momentum. That creates frustration among retail holders, especially those who expected a straightforward post-data move. It also creates opportunity for short-term traders who specialize in post-offering setups, but that is trading structure, not a fundamental conclusion.