SpaceX (Nasdaq: $SPCX): la festa e’ durata quattro giorni. Poi il conto.

1. La corsa e il muro: dieci giorni che hanno diviso il mercato

SpaceX e’ arrivata sul Nasdaq come un evento finanziario e culturale insieme. Non era una normale IPO tecnologica. Era il momento in cui il mercato pubblico poteva finalmente comprare un pezzo diretto del racconto piu’ potente costruito da Elon Musk: lanci riutilizzabili, Starlink, Starship, difesa, connettivita’ globale, AI infrastrutturale e, sullo sfondo, Marte.

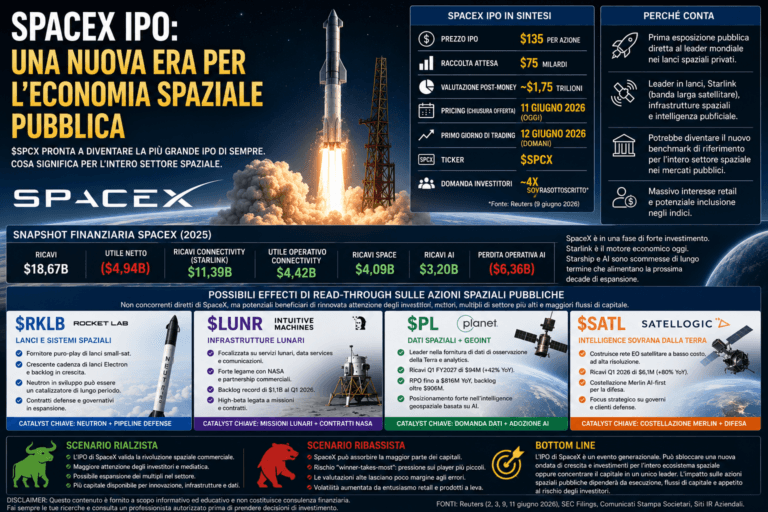

Il pricing ufficiale dell’offerta e’ stato fissato a $135 per azione per 555,555,555 azioni di classe A, pari a quasi $75 miliardi di raccolta primaria. L’over-allotment previsto era di 83,333,333 azioni aggiuntive; dopo l’esercizio del greenshoe, diverse fonti hanno riportato una raccolta complessiva arrivata a circa $85.7 miliardi. Questo passaggio e’ essenziale: non bisogna mischiare il numero base del prospetto con il numero successivo post-greenshoe.

La prima seduta ha confermato l’enorme domanda: titolo in rialzo vicino al 19%, chiusura intorno a $160.95/$161, retail molto presente e volume da evento sistemico. Ma il rally non si e’ fermato al debutto. Il 16 giugno SPCX ha toccato $225.64 intraday, arrivando a una capitalizzazione indicata da alcune ricostruzioni vicino ai $3 trilioni nei momenti di picco. Il punto e’ che quella quotazione non incorporava solo il business attuale: incorporava un premio enorme sulla possibilita’ che SpaceX diventi contemporaneamente infrastruttura spaziale, rete broadband globale, piattaforma AI e contractor strategico per governi e difesa.

- 12 giugno — Debutto sul Nasdaq a $135 SpaceX inizia a tradare sotto il ticker SPCX. La raccolta base e’ di circa $75 miliardi, tutta primaria. La chiusura del primo giorno intorno a $161 rende immediatamente chiaro che la domanda iniziale supera l’offerta pubblica disponibile.

- 16 giugno — Picco a $225.64 e mercato in piena euforia Il titolo tocca il massimo intraday dopo una fase di accelerazione alimentata da retail, opzioni e narrativa Musk. Le opzioni registrano volumi estremamente elevati e rendono il titolo uno dei centri del trading momentum globale.

- 16 giugno — Annuncio del deal Anysphere/Cursor SpaceX annuncia l’acquisizione di Anysphere, la societa’ dietro Cursor, per circa $60 miliardi in azioni. Il deal viene letto come un uso aggressivo della nuova valuta azionaria post-IPO.

- 18 giugno — Prima vera frenata Dopo il rally, arrivano prese di profitto e maggiore attenzione alla valutazione. Il mercato inizia a pesare ricavi, perdite, CapEx, AI spending e struttura finanziaria.

- 22 giugno — Bond da almeno $20B e terza seduta negativa SpaceX entra sul mercato obbligazionario con una possibile emissione da almeno $20 miliardi per rifinanziare debito ponte e finanziare obiettivi aziendali generali. Il titolo scende ancora, con prezzo intraday intorno a $165.19.

La sintesi e’ semplice: il debutto ha confermato la forza del brand SpaceX, ma la settimana successiva ha ricordato al mercato che anche le aziende eccezionali devono essere valutate con numeri, capitale, rischio e tempi di monetizzazione. Il rally non e’ stato smentito perche’ SpaceX e’ diventata improvvisamente una cattiva societa’. E’ stato ridimensionato perche’ il mercato ha prezzato in quattro sedute una quota enorme di futuro.

2. Perche’ la correzione non e’ solo panico: il capitale e’ il vero tema

La domanda centrale non e’ se SpaceX abbia tecnologia reale. La risposta e’ si’. SpaceX ha una posizione industriale che pochi competitor possono avvicinare: Falcon 9 e’ il cavallo da lavoro del mercato dei lanci, Starlink e’ una rete satellitare commerciale gia’ scalata, Starship e’ il progetto che puo’ cambiare la curva dei costi se raggiunge affidabilita’ operativa, e la relazione con NASA, difesa e clienti governativi crea un fossato strategico che una semplice startup non puo’ replicare.

La domanda vera e’ diversa: quanta cassa serve per trasformare questa architettura in un business capace di giustificare una valutazione da megacap? I filing e le fonti finanziarie mostrano un quadro misto: ricavi 2025 a circa $18.67 miliardi, crescita del 33% anno su anno, ma perdita netta 2025 intorno a $4.9 miliardi e Q1 2026 ancora pesante. SpaceX aveva circa $15.9 miliardi di cassa a fine marzo 2026, poi l’IPO ha cambiato drasticamente la liquidita’, portando la cassa riportata dopo il deal sopra $100 miliardi.

Questa liquidita’ e’ enorme, ma non cancella il punto. SpaceX sta finanziando contemporaneamente Starship, Starlink di nuova generazione, infrastruttura AI, accordi di cloud capacity, espansione di data center e potenzialmente una piattaforma di AI enterprise dopo l’integrazione con Cursor. Sono progetti con ritorni potenzialmente giganteschi, ma anche con CapEx anticipato e ricavi differiti.

Il bond da almeno $20 miliardi non va letto automaticamente come segnale negativo. Per una societa’ con rating investment-grade, rifinanziare un bridge loan con debito piu’ strutturato puo’ essere razionale. Il problema e’ il contesto: dopo una IPO da record, il mercato si aspettava forse un periodo di digestione. Invece ha visto subito una maxi-acquisizione in azioni e una maxi-operazione sul debito. Da qui nasce la narrativa del capitale: SpaceX puo’ essere una delle aziende piu’ importanti del mondo, ma resta una macchina che assorbe risorse su scala fuori dal normale.

Il lato positivo

La raccolta primaria e il greenshoe rafforzano il bilancio, aumentano la liquidita’ e danno a SpaceX margine per finanziare progetti pluriennali senza dipendere subito dal mercato azionario.

Il lato delicato

Il mercato deve capire se il capitale viene investito in progetti con ritorni visibili o se l’azienda sta solo allargando il perimetro di rischio tra spazio, AI, debito e acquisizioni.

Il nodo valutazione

A multipli molto elevati sui ricavi, anche piccole delusioni su CapEx, margini, tempi di Starship o monetizzazione AI possono creare correzioni violente.

3. Wall Street: non e’ una discussione su SpaceX, e’ una discussione sul prezzo

La polarizzazione degli analisti nasce da un fatto: SpaceX puo’ essere contemporaneamente una societa’ industriale eccezionale e un titolo troppo caro in una determinata finestra di prezzo. Questa distinzione e’ fondamentale. Il mercato tende a trasformare tutto in tifo: bull contro bear, Musk contro short seller, futuro contro passato. Ma la valutazione non funziona cosi’.

Il campo bull guarda a SpaceX come a una piattaforma multi-mercato: lanci, broadband, difesa, logistica orbitale, AI, cloud capacity, data center spaziali e forse servizi che ancora non esistono. In questa lettura, il valore attuale non va misurato solo sui ricavi 2025, ma sulla possibilita’ che SpaceX diventi un’infrastruttura globale quasi monopolistica in piu’ verticali.

Il campo bear non nega la qualita’ industriale. Contesta il multiplo, il cash burn, la complessita’ del conglomerato Musk e il rischio che il mercato stia pagando oggi ricavi che potrebbero materializzarsi molto piu’ tardi, con ulteriore debito e possibili diluizioni.

| Fonte / Osservatore | Taglio | Punto centrale | Implicazione per SPCX |

|---|---|---|---|

| SEC / prospetto | Base factual | Offerta primaria, struttura di classe A, greenshoe, dati finanziari e rischi ufficiali. | E’ la base piu’ importante: separa narrativa e numeri verificabili. |

| Reuters | News / market tape | IPO record, rally, volatilita’, bond, liquidita’ post-IPO, rating e debito. | Conferma che il mercato sta ricalibrando dopo euforia iniziale. |

| Morningstar | Valuation risk | Ricavi e perdite non bastano a giustificare valutazioni estreme se i flussi futuri richiedono troppo capitale. | Il titolo puo’ restare volatile fino a quando il mercato non vede cash conversion. |

| Damodaran | Valuation framework | SpaceX e’ unica, ma anche aziende uniche possono essere troppo care al prezzo sbagliato. | Il prezzo conta. Una buona azienda non e’ sempre un buon ingresso. |

| Retail / social | Momentum | La narrativa Musk, le opzioni e la scarsita’ di flottante hanno amplificato il movimento. | Aiuta a spiegare il rally, ma non sostituisce l’analisi fondamentale. |

4. Cursor/Anysphere: grande mossa strategica o uso aggressivo della valuta azionaria?

L’acquisizione da circa $60 miliardi di Anysphere, la societa’ dietro Cursor, e’ il passaggio che trasforma SPCX da semplice IPO spaziale a caso di studio su conglomerato tecnologico. Cursor e’ uno degli strumenti piu’ visibili nella corsa agli AI coding agents. Comprarlo significa cercare di portare dentro SpaceX un’interfaccia enterprise, un flusso di dati sviluppatori e un potenziale canale di distribuzione AI.

La logica bull e’ chiara: SpaceX non vuole solo usare AI internamente; vuole vendere capacita’, modelli, strumenti e infrastruttura. Cursor puo’ diventare un prodotto di front-end, mentre xAI/SpaceX forniscono modelli, compute, infrastruttura e integrazione. In questa lettura il deal e’ costoso, ma coerente con l’ambizione di trasformare SpaceX in una piattaforma AI fisica e software.

La logica bear e’ altrettanto chiara: $60 miliardi sono una cifra enorme per una societa’ giovane, anche in un mercato AI caldissimo. Pagare tutto in azioni riduce l’uso di cassa, ma aumenta la diluizione e lega il successo dell’operazione al livello del titolo. Se SPCX scende, il mercato puo’ leggere il deal come un uso opportunistico del picco post-IPO piu’ che come una transazione disciplinata.

Il rischio regolatorio non va ignorato. Un’acquisizione di queste dimensioni in AI coding, con coinvolgimento di una megacap appena quotata e legami con infrastruttura compute, puo’ attirare attenzione antitrust. Anche se il deal arrivasse a closing, l’integrazione tra cultura startup, AI product velocity e struttura industriale SpaceX non e’ automatica.

5. Retail sentiment: da “Musk premium” a “dove finisce il denaro?”

La piazza retail ha trattato SPCX come un evento piu’ che come un semplice titolo. Il primo movimento e’ stato dominato da scarsita’, FOMO e opzioni. Il secondo movimento, quello della correzione, e’ stato dominato da una domanda piu’ fredda: se l’azienda ha appena raccolto decine di miliardi, perche’ il mercato sente subito parlare di bond, bridge loan, CapEx e acquisizioni?

Questa non e’ una domanda superficiale. Nei titoli ad altissima narrativa il retail spesso accetta valutazioni estreme se vede una storia lineare: raccolta, crescita, margini futuri. Qui la storia e’ piu’ complessa: raccolta record, debito, AI spending, Cursor, Starship, Starlink, xAI, governance Musk, classi azionarie e rischio di capitale continuo.

Tesi retail bull

SpaceX domina i lanci, Starlink puo’ diventare una utility globale, Starship puo’ abbattere i costi, Cursor porta AI enterprise, Musk ha gia’ ribaltato mercati che sembravano impossibili.

Tesi retail bear

La valutazione anticipa troppi successi, il cash burn e’ elevato, il bond arriva troppo presto psicologicamente e il deal Cursor sembra fatto usando azioni gonfiate dal rally.

Opzioni

L’avvio delle opzioni ha creato una nuova struttura tecnica: non solo call speculative, ma anche puts, hedging, gamma e possibilita’ di pressione bidirezionale piu’ violenta.

Float e scarsita’

Un’offerta primaria enorme puo’ convivere con flottante iniziale relativamente stretto rispetto alla domanda globale. Questo amplifica movimenti sia al rialzo sia al ribasso.

Per il lettore trader, il retail sentiment e’ utile come termometro, non come prova. Quando il sentiment gira su un titolo appena quotato e iper-mediatico, il prezzo puo’ muoversi molto piu’ velocemente dei fondamentali. Ma se il sentiment resta negativo mentre il bond viene collocato bene e arrivano dati operativi solidi, il mercato puo’ anche costruire una base. La prossima fase sara’ meno narrativa e piu’ legata a dati: spread del bond, update su Cursor, Q2, guidance e contratti.

6. I rischi strutturali da monitorare

1. Valutazione e multipli

Il primo rischio e’ il piu’ banale e il piu’ importante: anche una societa’ straordinaria puo’ essere sopravvalutata. A valutazioni da megacap globale, il mercato non sta pagando solo SpaceX di oggi. Sta pagando Starlink a piena scala, Starship operativa, AI monetizzata, difesa in espansione e capitale disponibile a costi sostenibili.

2. CapEx e free cash flow

La traiettoria di cassa resta il nodo fondamentale. Se i ricavi crescono ma il CapEx cresce piu’ velocemente, il mercato continuera’ a chiedere finanziamenti. Il bond da almeno $20 miliardi puo’ essere efficiente, ma ogni round di capitale aumenta il controllo degli investitori sui numeri futuri.

3. Diluzione da stock deals

Pagare Cursor in azioni evita di usare cassa, ma non e’ gratis. Significa trasferire una parte dell’equity futura agli azionisti di Anysphere. Se SpaceX continuasse a usare il titolo come moneta per acquisizioni, gli investitori dovrebbero valutare non solo crescita e sinergie, ma anche diluizione cumulativa.

4. Governance e dual-class

La struttura di voto concentrata su Musk puo’ essere un vantaggio strategico, perche’ permette decisioni rapide e visione di lungo periodo. Ma per il mercato pubblico e’ anche un rischio: minor influenza degli azionisti ordinari, dipendenza dal fondatore e possibile conflitto di attenzione tra SpaceX, Tesla, xAI, X e altri progetti.

5. Regolatorio e geopolitico

SpaceX opera in aree sensibili: spazio, telecomunicazioni, difesa, AI e infrastruttura. Questo porta vantaggi enormi nei contratti governativi, ma anche rischi regolatori, export control, sicurezza nazionale, antitrust e dipendenza da relazioni politiche.

6. Effetto sui peer spaziali

Il debutto di SPCX puo’ drenare capitale dai peer piu’ piccoli nel breve periodo, perche’ molti investitori vendono proxy spaziali per comprare il nome principale. Ma se SpaceX corregge troppo, parte del capitale potrebbe tornare su RKLB, PL, ASTS, LUNR, SATL e altri nomi collegati alla filiera. La direzione dipendera’ dalla percezione: SpaceX come validazione del settore o SpaceX come aspiratore di liquidita’.

7. Catalysts da seguire adesso

| Catalyst | Finestra | Perche’ conta | Lettura trader |

|---|---|---|---|

| Pricing finale del bond | Settimana del 22 giugno | Mostra il costo reale del capitale e la domanda istituzionale per il credito SpaceX. | Spread contenuti = supporto alla tesi investment-grade; spread larghi = pressione su equity. |

| Chiusura / aggiornamenti Cursor | Q3 2026 atteso | Verifica rischio regolatorio, struttura del deal e narrativa AI enterprise. | Qualsiasi ritardo o richiesta antitrust puo’ pesare sul titolo. |

| Q2 2026 results | Fine luglio 2026 attesa | Primo vero test da societa’ pubblica dopo IPO. | Mercato guardera’ revenue growth, net loss, FCF, CapEx, cash balance e guidance. |

| Index inclusion / passive flows | Fine giugno / prossime revisioni | Una mega IPO liquida puo’ essere candidata a inclusioni accelerate in indici e ETF. | Potenziale domanda tecnica, ma non sostituisce fondamentali. |

| Contratti governativi / difesa | Continuo | NASA, DoD e contratti satellitari possono rafforzare la tesi di infrastruttura strategica. | News forti possono cambiare sentiment rapidamente. |

| Starship milestones | 2026 | Starship e’ la chiave della curva costi e della visione long-term. | Successi operativi aiutano il multiplo; ritardi pesano sulla narrativa. |

8. Scenari possibili

Scenari descrittivi a scopo educativo. Non sono raccomandazioni operative.

- Bond collocato con domanda forte e spread ragionevoli.

- Q2 mostra ricavi in crescita, cash burn sotto controllo e liquidita’ solida.

- Cursor ottiene via libera regolatorio senza condizioni pesanti.

- Starlink accelera utenti, ARPU o contratti enterprise/governativi.

- Index inclusion crea domanda passiva aggiuntiva.

- Il titolo costruisce base sopra area IPO e recupera gradualmente credibilita’.

- Bond collocato, ma senza entusiasmo estremo.

- Il titolo resta volatile tra prezzo IPO e area post-rally.

- Q2 conferma crescita ma anche forte CapEx.

- Cursor resta una promessa piu’ che un contributore immediato.

- Mercato passa da FOMO a valutazione piu’ disciplinata.

- Spread del bond piu’ alti del previsto o domanda meno solida.

- Q2 mostra burn rate ancora in accelerazione.

- Regolatori rallentano o contestano il deal Cursor.

- Lock-up e vendite pre-IPO creano pressione tecnica.

- Il titolo perde area IPO e la narrativa retail si trasforma in capitolazione.

9. Merlintrader bottom line

SpaceX e’ probabilmente una delle societa’ piu’ importanti mai arrivate sul mercato pubblico. Ma proprio per questo non va trattata come una meme stock qualsiasi. La tecnologia e’ reale, la posizione competitiva e’ reale, il ruolo strategico e’ reale. Anche i rischi sono reali: valutazione, CapEx, debito, diluizione, governance e tempi di monetizzazione AI.

Il mercato ha fatto in pochi giorni quello che spesso fa con le grandi IPO narrative: prima ha comprato la storia, poi ha iniziato a leggere il prospetto. A $225 il prezzo stava trattando SpaceX come se quasi tutto il futuro fosse gia’ risolto. In area $165 il titolo resta sopra l’IPO price, ma la conversazione e’ cambiata: non piu’ solo “quanto puo’ diventare grande SpaceX?”, ma “quanto capitale servira’ per arrivarci, e quanto ritorno restera’ agli azionisti comuni?”.

La vera verifica arrivera’ con il bond, con Q2 e con i primi dettagli concreti sull’integrazione Cursor. Fino ad allora, SPCX resta uno dei titoli piu’ importanti e piu’ difficili da leggere del mercato 2026: enorme qualita’ industriale, enorme premio narrativo, enorme bisogno di disciplina nella valutazione.

1. The run and the wall: ten days that split the market

SpaceX arrived on Nasdaq as both a financial event and a cultural event. This was not a normal technology IPO. It was the moment when public-market investors could finally buy a direct piece of Elon Musk’s most powerful industrial story: reusable rockets, Starlink, Starship, defense, global connectivity, infrastructure AI and, in the background, Mars.

The official offering was priced at $135 per share for 555,555,555 Class A shares, equal to almost $75 billion in primary proceeds. The over-allotment option covered another 83,333,333 shares; after the greenshoe, recent sources have reported total proceeds of roughly $85.7 billion. That distinction matters: the base prospectus number and the post-greenshoe number should not be blended without explanation.

The first session confirmed extraordinary demand: the stock rose roughly 19%, closed around $160.95/$161, retail participation was intense and volume behaved like a systemic market event. But the rally did not stop on day one. On June 16, SPCX hit an intraday high of $225.64, with some market-cap reconstructions putting the company close to $3 trillion at the peak. That price was not simply valuing the current business. It was valuing a giant optionality package across space infrastructure, broadband, AI, defense and long-term orbital compute.

- June 12 — Nasdaq debut at $135 SpaceX begins trading under SPCX. The base offering is around $75 billion, all primary. A first-day close around $161 immediately confirms that initial demand exceeds available public supply.

- June 16 — Peak at $225.64 The stock reaches its intraday high after a momentum acceleration fueled by retail demand, options activity and the Musk premium.

- June 16 — Cursor/Anysphere deal announced SpaceX announces the acquisition of Anysphere, the company behind Cursor, for roughly $60 billion in stock.

- June 18 — First real cooling phase After the rally, profit-taking and valuation discipline begin to matter. Investors refocus on revenue, losses, CapEx, AI spending and capital structure.

- June 22 — $20B+ bond plan and another down session SpaceX enters the bond market with a potential offering of at least $20 billion to refinance bridge debt and fund general corporate purposes. The stock trades intraday around $165.19.

The short version is that the IPO confirmed the strength of the SpaceX brand, but the following week reminded the market that even exceptional companies must still be valued through numbers, capital needs, risk and monetization timelines. The rally was not questioned because SpaceX suddenly became a poor company. It was questioned because the market priced a very large amount of future success in only a few sessions.

2. Why the pullback is not just panic: capital is the real issue

The core question is not whether SpaceX has real technology. It clearly does. The company has an industrial position few competitors can approach: Falcon 9 is the workhorse of commercial launch, Starlink is already a scaled satellite network, Starship could change the cost curve if it reaches operational reliability, and relationships with NASA, defense and government customers create a strategic moat that a standard startup cannot replicate.

The real question is different: how much cash is required to convert this architecture into a business capable of justifying a mega-cap valuation? Filings and financial reports show a mixed picture: 2025 revenue of roughly $18.67 billion, 33% year-over-year growth, a 2025 net loss around $4.9 billion, and a still-heavy first quarter of 2026. SpaceX held about $15.9 billion in cash at the end of March 2026, then the IPO dramatically changed liquidity, pushing reported cash after the deal above $100 billion.

That liquidity is enormous, but it does not eliminate the issue. SpaceX is funding Starship, next-generation Starlink, AI infrastructure, cloud-capacity agreements, data-center expansion and potentially an enterprise AI platform after the Cursor integration. These projects may create giant returns, but they also require front-loaded CapEx and deferred revenue realization.

The $20 billion-plus bond plan should not be read automatically as negative. For an investment-grade company, refinancing a bridge loan with longer-term debt can be rational. The problem is context: after a record IPO, the market may have expected a digestion period. Instead, it immediately saw a major stock acquisition and a major debt transaction. That is why the capital narrative matters: SpaceX may be one of the most important companies in the world, but it remains a machine that absorbs resources on an extraordinary scale.

The positive side

The primary raise and greenshoe strengthen the balance sheet, increase liquidity and give SpaceX more room to fund multi-year projects without immediately depending on equity markets.

The delicate side

Investors need to understand whether capital is being invested into visible-return projects or whether the company is expanding the risk perimeter across space, AI, debt and acquisitions.

The valuation node

At very high revenue multiples, even small disappointments in CapEx, margins, Starship timing or AI monetization can create violent corrections.

3. Wall Street: this is not a debate about SpaceX, it is a debate about price

The analyst split comes from one reality: SpaceX can be an exceptional industrial company and still be too expensive at a specific price. That distinction is crucial. Markets often turn everything into tribal arguments: bulls versus bears, Musk versus short sellers, future versus past. Valuation is less emotional than that.

The bullish camp sees SpaceX as a multi-market platform: launch, broadband, defense, orbital logistics, AI, cloud capacity, space-based data centers and perhaps services that do not yet exist. In this reading, current value should not be measured only against 2025 revenue, but against the possibility that SpaceX becomes a quasi-monopolistic global infrastructure layer across several verticals.

The bearish camp does not deny the industrial quality. It challenges the multiple, cash burn, Musk-conglomerate complexity and the risk that markets are paying today for revenues that may arrive much later, after more debt and potential dilution.

| Source / observer | Angle | Core point | Implication for SPCX |

|---|---|---|---|

| SEC / prospectus | Factual base | Primary offering, Class A structure, greenshoe, financials and official risks. | The most important base layer: it separates narrative from verified data. |

| Reuters | Market tape | Record IPO, rally, volatility, bond, post-IPO liquidity, ratings and debt. | Confirms that markets are recalibrating after the initial euphoria. |

| Morningstar | Valuation risk | Revenue and losses do not automatically justify extreme valuations if future cash flows require too much capital. | The stock can remain volatile until cash conversion becomes clearer. |

| Damodaran | Valuation framework | SpaceX is unique, but unique companies can still be overpriced at the wrong entry point. | Price matters. A great company is not always a great purchase at every price. |

| Retail / social | Momentum | The Musk narrative, options and limited initial float amplified the move. | Useful for explaining the rally, but not a substitute for fundamental analysis. |

4. Cursor/Anysphere: strategic move or aggressive use of stock currency?

The roughly $60 billion acquisition of Anysphere, the company behind Cursor, is the step that turns SPCX from a space IPO into a case study in technology-conglomerate strategy. Cursor is one of the most visible products in the AI coding-agent race. Buying it means bringing an enterprise interface, developer-data flow and potential AI distribution channel inside SpaceX.

The bull logic is clear: SpaceX does not simply want to use AI internally; it wants to sell capacity, models, tools and infrastructure. Cursor can become a front-end product while xAI/SpaceX provide models, compute, infrastructure and integration. In that reading, the deal is expensive but coherent with the ambition to turn SpaceX into a physical and software AI platform.

The bear logic is equally clear: $60 billion is a huge number for a young company, even in a very hot AI market. Paying entirely in stock saves cash, but increases dilution and links the deal’s economics to the share price. If SPCX keeps falling, investors may interpret the deal as opportunistic use of post-IPO euphoria rather than disciplined capital allocation.

Regulatory risk should not be ignored. A deal of this size in AI coding, involving a newly listed mega-cap and compute infrastructure, can attract antitrust attention. Even if the transaction closes, integrating startup product velocity with SpaceX’s industrial structure is not automatic.

5. Retail sentiment: from “Musk premium” to “where does the money go?”

Retail treated SPCX as an event rather than a normal stock. The first move was dominated by scarcity, FOMO and options. The second move, the pullback, was dominated by a colder question: if the company just raised tens of billions, why is the market immediately hearing about bonds, bridge loans, CapEx and acquisitions?

That is not a shallow question. In high-narrative stocks, retail investors often accept extreme valuations if the story looks linear: raise, growth, future margins. Here the story is more complex: record raise, debt, AI spending, Cursor, Starship, Starlink, xAI, Musk governance, share classes and the risk of ongoing capital demand.

Retail bull thesis

SpaceX dominates launch, Starlink can become a global utility, Starship can lower the cost curve, Cursor brings enterprise AI, and Musk has already upended markets that looked impossible.

Retail bear thesis

The valuation anticipates too many wins, cash burn is high, the bond comes too soon psychologically, and the Cursor deal looks like it was paid for with stock inflated by the rally.

Options

The launch of options created a new technical structure: not only speculative calls, but also puts, hedging, gamma effects and stronger two-way pressure.

Float and scarcity

A giant primary offering can still coexist with limited initial free float relative to global demand. That amplifies moves in both directions.

For traders, retail sentiment is useful as a thermometer, not as proof. When sentiment turns on a newly listed, hyper-visible stock, price can move much faster than fundamentals. But if sentiment stays weak while the bond is placed well and operating data holds up, the market can still build a base. The next phase will be less about narrative and more about data: bond spreads, Cursor updates, Q2, guidance and contracts.

6. Structural risks to monitor

1. Valuation and multiples

The first risk is the most basic and the most important: even an extraordinary company can be overvalued. At global mega-cap valuations, markets are not paying only for today’s SpaceX. They are paying for scaled Starlink, operational Starship, monetized AI, defense expansion and sustainable access to capital.

2. CapEx and free cash flow

The cash trajectory remains the central issue. If revenue grows but CapEx grows faster, the market will continue to demand financing. The $20 billion-plus bond may be efficient, but each funding event increases investor focus on future numbers.

3. Dilution from stock deals

Paying for Cursor in stock avoids using cash, but it is not free. It transfers part of future equity value to Anysphere shareholders. If SpaceX keeps using the stock as acquisition currency, investors must analyze cumulative dilution alongside growth and synergies.

4. Governance and dual class

Musk’s concentrated voting power can be a strategic advantage, enabling fast decisions and long-term vision. For public markets it is also a risk: ordinary shareholders have less influence, the founder is central, and attention can be spread across SpaceX, Tesla, xAI, X and other projects.

5. Regulatory and geopolitical risk

SpaceX operates in sensitive areas: space, telecommunications, defense, AI and infrastructure. That creates major advantages in government contracts, but also regulatory, export-control, national-security, antitrust and political-dependency risks.

6. Spillover into smaller space peers

SPCX’s debut can drain capital from smaller space peers in the short term because investors may sell proxies to buy the primary name. But if SpaceX corrects too far, some capital can return to RKLB, PL, ASTS, LUNR, SATL and other space-chain names. The direction depends on perception: SpaceX as sector validation or SpaceX as a liquidity vacuum.

7. Catalysts to watch now

| Catalyst | Window | Why it matters | Trader read-through |

|---|---|---|---|

| Final bond pricing | Week of June 22 | Shows the real cost of capital and institutional credit demand for SpaceX. | Tight spreads support the investment-grade thesis; wide spreads pressure equity. |

| Cursor closing / updates | Expected Q3 2026 | Tests regulatory risk, deal structure and enterprise AI narrative. | Delays or antitrust requests can weigh on the stock. |

| Q2 2026 results | Expected late July 2026 | First real public-company test after the IPO. | Market will focus on revenue growth, net loss, FCF, CapEx, cash balance and guidance. |

| Index inclusion / passive flows | Late June / upcoming reviews | A liquid mega IPO can become a candidate for accelerated index and ETF inclusion. | Possible technical demand, but not a substitute for fundamentals. |

| Government / defense contracts | Ongoing | NASA, DoD and satellite contracts can reinforce the strategic-infrastructure thesis. | Strong news can quickly shift sentiment. |

| Starship milestones | 2026 | Starship is central to the cost curve and long-term vision. | Operational success supports the multiple; delays pressure the narrative. |

8. Possible scenarios

Descriptive analytical scenarios for educational purposes only. Not investment advice.

- Bond placed with strong demand and reasonable spreads.

- Q2 shows revenue growth, controlled cash burn and strong liquidity.

- Cursor receives regulatory clearance without heavy conditions.

- Starlink accelerates users, ARPU or government/enterprise contracts.

- Index inclusion creates additional passive demand.

- The stock builds a base above IPO price and gradually restores credibility.

- Bond is placed, but without extreme enthusiasm.

- The stock remains volatile between IPO price and the post-rally zone.

- Q2 confirms growth but also heavy CapEx.

- Cursor remains a promise rather than an immediate contributor.

- Market shifts from FOMO to more disciplined valuation.

- Bond spreads are higher than expected or demand is less solid.

- Q2 shows cash burn still accelerating.

- Regulators slow or challenge the Cursor deal.

- Lock-up and pre-IPO selling create technical pressure.

- The stock loses IPO-price area and retail narrative turns into capitulation.

9. Merlintrader bottom line

SpaceX is probably one of the most important companies ever to enter public markets. That is exactly why it should not be treated like a normal meme stock. The technology is real, the competitive position is real, and the strategic role is real. The risks are also real: valuation, CapEx, debt, dilution, governance and AI monetization timing.

In only a few days, the market did what it often does with narrative IPOs: first it bought the story, then it started reading the prospectus. At $225, the price was treating SpaceX as if most of the future had already been solved. Around $165, the stock remains above IPO price, but the conversation has changed: no longer just “how big can SpaceX become?”, but “how much capital will it take to get there, and how much return will remain for common shareholders?”.

The real test will come through the bond, Q2 results and concrete details around Cursor integration. Until then, SPCX remains one of the most important and most difficult stocks to read in the 2026 market: enormous industrial quality, enormous narrative premium and enormous need for valuation discipline.

Il presente contenuto e’ redatto da Merlintrader a puro scopo informativo ed educativo. Non costituisce sollecitazione al pubblico risparmio, consulenza finanziaria, raccomandazione di investimento ne’ offerta di strumenti finanziari ai sensi del D.Lgs. 58/1998 (TUF) e delle disposizioni CONSOB vigenti, ne’ ai sensi del Securities Act of 1933 e dello Securities Exchange Act of 1934 (SEC/USA). I dati e le informazioni riportati provengono da fonti ritenute attendibili, incluse fonti ufficiali, filing SEC, comunicati aziendali e principali agenzie di stampa, ma non se ne garantisce la completezza o accuratezza. Investire in strumenti finanziari comporta rischi, inclusa la perdita totale del capitale investito. Prima di prendere qualsiasi decisione di investimento, consultare un advisor finanziario autorizzato. Per il disclaimer completo: merlintrader.eu/disclaimer

Biotech & Tech Catalyst Calendar

Tutti i catalyst: PDUFA, trial readout, earnings, IPO lock-up expiry, market events

Vai al Catalyst Calendar