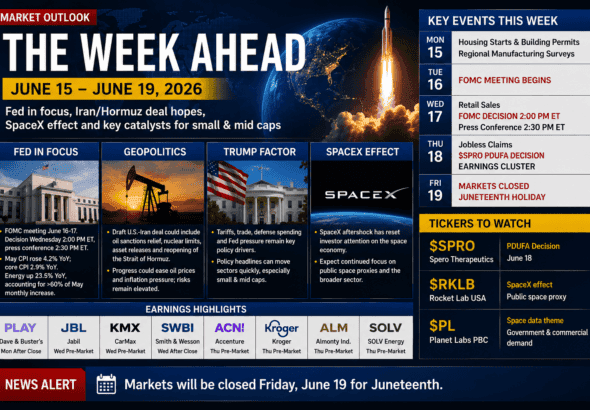

Daily Briefing – 18 giugno: Fed hawkish, petrolio in calo dopo USA-Iran/Hormuz, Intel corre sul tema Apple, SpaceX digerisce l’IPO, MRVL/FLEX restano nel flusso S&P 500 e SPRO affronta il PDUFA

Il briefing del 18 giugno mantiene il focus principale sugli Stati Uniti, ma con lettura diretta anche per Italia ed Europa. Il mercato sta digerendo due forze opposte: da una parte il petrolio più basso dopo l’accordo interinale USA-Iran e la riapertura attesa dello Stretto di Hormuz; dall’altra una Federal Reserve più hawkish dopo il primo meeting di Kevin Warsh come presidente. I futures USA rimbalzano grazie all’ottimismo geopolitico e alla forza dei semiconduttori, con Intel in forte rialzo dopo le dichiarazioni su una possibile collaborazione con Apple per progettare e produrre chip negli Stati Uniti. SpaceX resta il termometro del rischio retail, ma entra nella fase di digestione dopo la prima vera pausa post-IPO. Marvell e Flex restano catalyst tecnici in vista dell’ingresso nello S&P 500 prima dell’apertura del 22 giugno. In biotech, SPRO/GSK sono il binary watch del giorno con il PDUFA FDA per tebipenem HBr nelle infezioni urinarie complicate.

- INTC— Intel è il mover più pulito della mattinata dopo le dichiarazioni di Trump su una collaborazione Apple-Intel per progettare e produrre chip negli Stati Uniti. Il titolo è salito con forza nel premarket e riporta al centro reshoring, foundry strategy, semiconduttori USA e politica industriale.Chip Deal

- AAPL / INTC— Apple entra nella lettura perché una partnership produttiva con Intel toccherebbe supply chain, sicurezza dei chip, capacità manifatturiera domestica e dipendenza da fornitori esteri. Per ora resta una headline potente, ma il mercato dovrà vedere dettagli commerciali, volumi, timing e margini.Apple / Chips

- MU / MRVL / NVDA— Micron, Marvell e Nvidia sono i primi controlli sulla ripartenza dei semiconduttori dopo lo shock Fed. Il gruppo deve dimostrare che il trade AI può reggere anche con aspettative sui tassi meno favorevoli.AI Semis

- MRVL / FLEX— Marvell e Flex restano catalyst tecnici reali perché S&P Dow Jones Indices ha programmato l’ingresso di entrambi nello S&P 500 prima dell’apertura del 22 giugno 2026. Il tema resta flusso passivo, ribilanciamento ETF, benchmark demand, liquidità e posizionamento.Index Flow

- MRVL— Marvell ha la narrativa più forte della coppia perché combina ingresso nello S&P 500, custom silicon, networking per data center e seconda linea dell’infrastruttura AI. Se SOXX stabilizza, MRVL resta uno dei crossover più interessanti tra AI e index-flow.AI / Index

- FLEX— Flex porta nel ribilanciamento la parte industrial technology e produzione elettronica. È meno spettacolare di Marvell, ma resta rilevante per supply chain, hardware AI, manifattura e flussi benchmark.Industrial Tech

- SPCX— SpaceX resta il termometro più pulito dell’appetito retail per il rischio, ma il tono è cambiato. Dopo il debutto record e la corsa iniziale, il titolo è nella fase di digestione: il punto ora è capire se i compratori difendono i ribassi o se la narrativa IPO si trasforma in trade troppo affollato.Space IPO

- SPCX Options— Le opzioni su SpaceX restano un layer meccanico importante. La domanda di call può sostenere il momentum, ma gli stessi flussi possono produrre inversioni veloci quando cambiano coperture, gamma e liquidità intraday.Options

- RKLB / LUNR / PL / SATL— Il paniere space quotato resta in verifica post-SpaceX. Il debutto di SpaceX valida il tema, ma non valida automaticamente ogni titolo del settore. RKLB, LUNR, PL e SATL devono mostrare forza relativa propria, non solo simpatia da headline.Space Basket

- JBL— Jabil resta in evidenza dopo un report beat-and-raise sostenuto dalla domanda AI infrastructure. È una lettura concreta perché misura server, componenti, produzione, margini e conversione degli ordini, non solo narrativa AI.AI Infra

- DELL / HPE / SMCI— I server AI restano il checkpoint della domanda reale. Il mercato vuole ordini, margini, backlog convertito e deployment enterprise, non soltanto narrativa.AI Servers

- VRT / ETN / GEV— Power e cooling restano letture strutturali dell’infrastruttura AI. Data center, elettricità, sottostazioni, raffreddamento e backup power sono il lato più concreto del secondo ordine AI.Power / Cooling

- ORCL— Oracle resta la lezione sul capex AI. Il mercato ama backlog cloud e domanda AI, ma continua a chiedersi quanto debito, capex e free cash flow negativo siano accettabili in cambio della crescita infrastrutturale.AI Capex

- RUM / SWBI— Rumble e Smith & Wesson sono mover speculativi/earnings da monitorare. RUM resta una lettura retail/AI-media, mentre SWBI segnala che anche gli earnings single-stock possono attirare flussi in una giornata dominata da macro.Movers

- AAL / DAL / UAL / CCL / RCL— Airlines e cruise ricevono ossigeno dal petrolio più basso e dal minore stress geopolitico. Il trade migliora se crude resta contenuto e Hormuz normalizza; si indebolisce se la Fed colpisce consumer cyclicals o se il petrolio rimbalza.Travel / Oil

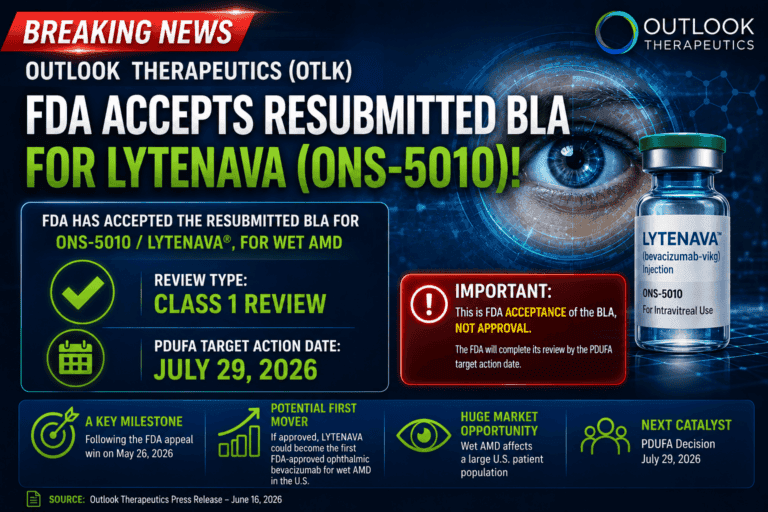

- SPRO / GSK— Spero e GSK sono il binary biotech del giorno, con PDUFA FDA al 18 giugno 2026 per tebipenem HBr nelle infezioni urinarie complicate, inclusa pielonefrite. Approvazione, ritardo o CRL possono cambiare rapidamente la lettura del trade.PDUFA Today

- VRDN— Viridian resta uno dei catalyst biotech più chiari di fine giugno, con veligrotug in Priority Review FDA e PDUFA target date al 30 giugno 2026 per thyroid eye disease.PDUFA Watch

- COGT— Cogent resta una storia post-EHA da monitorare. I dati APEX su bezuclastinib in mastocitosi sistemica avanzata hanno dato al mercato un catalyst concreto; ora contano qualità della reazione, timing NDA e durata della narrativa clinica.EHA / Data

- Fed hangover— La Fed ha lasciato i tassi fermi, ma il messaggio è stato abbastanza hawkish da cambiare il tono del mercato. Warsh ha riportato il focus su inflazione, credibilità e rischio di tassi più alti più a lungo.Fed

- Petrolio in calo— Il Brent è sceso verso l’area alta dei $70 dopo l’accordo interinale USA-Iran e la riapertura attesa di Hormuz. Questo aiuta la psicologia dell’inflazione, ma il mercato deve ancora verificare flussi fisici, assicurazioni e normalizzazione delle rotte.Oil

- Hormuz resta il test pratico— Rotte navali, assicurazioni, sicurezza, backlog e normalizzazione fisica dei flussi contano più degli slogan politici. È lì che il trade sul petrolio verrà confermato o smentito.Shipping

- Dollaro e rendimenti— Il dollaro più fermo e rendimenti più alti possono limitare il sollievo generato dal petrolio più basso. Per growth, biotech e small caps, la vera conferma arriva da TLT, DXY, IWM e XBI.Rates / FX

- Tech prova il rimbalzo— Intel aiuta la narrativa chip, ma SOXX e QQQ devono confermare con breadth vera. Un rimbalzo solo da headline non basta se Nvidia, Micron, Marvell, Broadcom, AMD e Arm non partecipano.Tech

- Settimana di scadenze— Triple witching, settimana USA accorciata, opzioni SpaceX, Fed e ribilanciamenti S&P aumentano la probabilità di swing intraday anche se la narrativa macro resta costruttiva.Volatility

Daily Briefing – June 18: Hawkish Fed Hangover, Oil Slides After U.S.–Iran/Hormuz Relief, Intel Jumps on Apple Chip Headlines, SpaceX Digests the IPO Surge, MRVL/FLEX Stay in the S&P 500 Flow Window, and SPRO Faces FDA Decision Day

The June 18 briefing keeps the main focus on the United States, with a direct read-through for Italy and Europe. The market is digesting two opposite forces at the same time: lower oil after the U.S.–Iran interim agreement and the expected reopening of the Strait of Hormuz, and a more hawkish Federal Reserve after Kevin Warsh’s first meeting as chair. U.S. futures are rebounding as geopolitical optimism and semiconductor strength offset rate concerns, with Intel sharply higher after comments about a possible Apple partnership to design and manufacture chips in the United States. SpaceX remains the retail-risk thermometer, but it has moved into the first digestion phase after the post-IPO surge. Marvell and Flex remain technical catalysts ahead of their scheduled S&P 500 additions before the June 22 open. In biotech, SPRO/GSK are the day’s binary watch with the FDA PDUFA date for tebipenem HBr in complicated urinary tract infections.

- INTC— Intel is the cleanest fresh mover after Trump said Apple would work with Intel to design and manufacture chips in the United States. The stock jumped sharply in premarket trading and puts reshoring, foundry strategy, U.S. semiconductor capacity and industrial policy back at the center of the tape.Chip Deal

- AAPL / INTC— Apple matters because any Intel manufacturing partnership would touch supply-chain resilience, chip security, domestic manufacturing capacity and dependence on overseas suppliers. For now, this is a powerful headline, but the market still needs commercial details, volumes, timing and margins.Apple / Chips

- MU / MRVL / NVDA— Micron, Marvell and Nvidia are the first semiconductor rebound checks after the Fed shock. The group needs to prove that the AI trade can still attract buyers even with less favorable rate expectations.AI Semis

- MRVL / FLEX— Marvell and Flex remain real technical catalysts because S&P Dow Jones Indices has scheduled both additions to the S&P 500 before the June 22, 2026 open. The setup is still about passive demand, ETF rebalancing, benchmark flows, liquidity and positioning.Index Flow

- MRVL— Marvell has the stronger narrative inside the rebalance pair because it combines S&P 500 inclusion, custom silicon, data-center networking and second-layer AI infrastructure exposure. If SOXX stabilizes, MRVL remains one of the cleaner AI/index-flow crossover trades.AI / Index

- FLEX— Flex brings the industrial-technology and electronics-manufacturing side of the rebalance. It is less flashy than Marvell, but still relevant for supply chains, AI hardware, manufacturing capacity and benchmark-driven demand.Industrial Tech

- SPCX— SpaceX remains the market’s cleanest retail-risk thermometer, but the tone has changed. After the record debut and early surge, the stock is now in digestion mode: the key is whether buyers defend pullbacks or whether the IPO narrative becomes too crowded.Space IPO

- SPCX Options— SpaceX options remain a major mechanical layer. Heavy call demand can support momentum, but the same flows can also create fast reversals when hedging, gamma and intraday liquidity shift.Options

- RKLB / LUNR / PL / SATL— The public space basket remains in a post-SpaceX verification phase. SpaceX validates the theme, but it does not automatically validate every listed space name. RKLB, LUNR, PL and SATL need independent relative strength, not only headline sympathy.Space Basket

- JBL— Jabil stays in focus after a beat-and-raise report supported by AI infrastructure demand. This is a concrete read because it measures servers, components, manufacturing, margins and order conversion, not only AI narrative.AI Infra

- DELL / HPE / SMCI— AI server names remain the real-demand checkpoint. The market wants orders, margins, backlog conversion and enterprise deployment, not only narrative momentum.AI Servers

- VRT / ETN / GEV— Power and cooling remain structural AI infrastructure reads. Data centers, electricity, substations, thermal management and backup power are among the most concrete second-order AI themes.Power / Cooling

- ORCL— Oracle remains the AI capex lesson. The market likes cloud backlog and AI demand, but investors are still asking how much capex, debt and negative free cash flow should be tolerated in exchange for infrastructure growth.AI Capex

- RUM / SWBI— Rumble and Smith & Wesson are speculative/earnings movers to monitor. RUM remains an AI-media and retail-risk read, while SWBI shows that single-stock earnings can still attract flows in a macro-dominated session.Movers

- AAL / DAL / UAL / CCL / RCL— Airlines and cruise names get oxygen from lower oil and reduced geopolitical stress. The trade improves if crude stays contained and Hormuz normalizes; it weakens if the Fed hits consumer cyclicals or oil rebounds.Travel / Oil

- SPRO / GSK— Spero and GSK are the biotech binary of the day, with the FDA PDUFA date on June 18, 2026 for tebipenem HBr in complicated urinary tract infections, including pyelonephritis. Approval, delay or CRL can quickly change the trade.PDUFA Today

- VRDN— Viridian remains one of the cleanest late-June biotech catalyst watches, with veligrotug under FDA Priority Review and a June 30, 2026 PDUFA target date in thyroid eye disease.PDUFA Watch

- COGT— Cogent remains a post-EHA follow-through story. The APEX data for bezuclastinib in advanced systemic mastocytosis gave the market a defined clinical catalyst; now the focus shifts to reaction quality, NDA timing and durability of the data narrative.EHA / Data

- Fed hangover— The Fed held rates steady, but the message was hawkish enough to change the market tone. Warsh has brought the focus back to inflation, credibility and the risk of higher-for-longer policy.Fed

- Oil slides— Brent has moved toward the high-$70s after the U.S.–Iran interim agreement and the expected reopening of Hormuz. That helps inflation psychology, but the market still needs to verify physical flows, insurance and route normalization.Oil

- Hormuz remains the practical test— Shipping routes, insurance, safety assurances, backlog clearance and physical flow normalization matter more than political slogans. That is where the oil-relief trade will be confirmed or rejected.Shipping

- Dollar and yields— A firmer dollar and higher yields can limit the relief created by lower oil. For growth, biotech and small caps, the real confirmation comes from TLT, DXY, IWM and XBI.Rates / FX

- Tech rebound attempt— Intel helps the chip narrative, but SOXX and QQQ need real breadth confirmation. A headline-only bounce is not enough if Nvidia, Micron, Marvell, Broadcom, AMD and Arm do not participate.Tech

- Expiration week mechanics— Triple witching, a shortened U.S. week, SpaceX options, Fed risk and S&P 500 rebalancing increase the probability of intraday swings even if the macro narrative remains constructive.Volatility