Daily Briefing – 17 giugno: Fed al centro, petrolio sotto $80, SpaceX diventa una macchina di volatilità, MRVL/FLEX restano nel flusso S&P 500 e l’Europa segue il segnale USA

Il briefing del 17 giugno mantiene il focus principale sugli Stati Uniti, perché oggi il mercato globale ruota attorno alla decisione della Federal Reserve. Il petrolio resta sotto quota $80 dopo il quadro diplomatico USA-Iran e le ipotesi di alleggerimento delle sanzioni sul greggio iraniano, ma la vera conferma arriverà solo da Hormuz, dalle assicurazioni sulle rotte, dai flussi fisici e dalla tenuta politica dell’accordo. SpaceX non è più soltanto la storia dell’IPO record: con le opzioni ora al centro dell’attenzione, SPCX è diventato un indicatore diretto di volatilità, domanda retail, gamma e appetito per il rischio high-beta. Marvell e Flex restano due catalyst tecnici importanti in vista dell’ingresso nello S&P 500 prima dell’apertura del 22 giugno. Per Italia ed Europa, il punto chiave è capire quanto il sollievo su petrolio e geopolitica possa sostenere FTSE MIB, banche, industriali, energia, semiconduttori europei, difesa e travel senza perdere il collegamento con il segnale macro USA.

- SPCX— SpaceX resta il termometro più pulito dell’appetito retail per il rischio. Dopo il debutto record al Nasdaq, il titolo è passato dalla semplice narrativa IPO a una storia di valutazione, flottante limitato, momentum e digestione della domanda. Il punto non è solo se il prezzo continua a salire, ma se la volatilità resta controllabile.Space IPO

- SPCX Options— Le opzioni su SpaceX aggiungono un layer meccanico importante. La domanda di call può sostenere il momentum, ma gli stessi flussi possono produrre inversioni violente quando cambiano coperture, gamma e liquidità intraday.Options

- RKLB / LUNR / PL / SATL— Il paniere space quotato resta in verifica post-SpaceX. Il debutto di SpaceX valida il tema, ma non valida automaticamente ogni titolo del settore. RKLB, LUNR, PL e SATL devono mostrare forza relativa propria, non solo simpatia da headline.Space Basket

- MRVL / FLEX— Marvell e Flex restano catalyst tecnici reali perché S&P Dow Jones Indices ha programmato l’ingresso di entrambi nello S&P 500 per il 22 giugno 2026. Il tema è flusso passivo, ribilanciamento ETF, benchmark demand, liquidità e posizionamento.Index Flow

- MRVL— Marvell ha la narrativa più forte della coppia perché combina ingresso nello S&P 500, custom silicon, networking per data center e seconda linea dell’infrastruttura AI. Il test è capire se il mercato vuole ancora AI exposure oltre i leader mega-cap.AI / Index

- FLEX— Flex porta nel ribilanciamento la parte industrial technology e produzione elettronica. È meno spettacolare di Marvell, ma rilevante per supply chain, hardware AI, manifattura e flussi benchmark.Industrial Tech

- NVDA— Nvidia resta l’ancora del trade AI. Se NVDA regge, l’AI può continuare a fare da spina dorsale del mercato. Se perde forza nel giorno Fed, i titoli secondari AI diventano più vulnerabili.AI Leader

- AVGO / MRVL / AMD / ARM— La breadth dei semiconduttori AI è uno dei controlli principali. Broadcom resta il benchmark custom silicon, Marvell aggiunge il tema index-flow, AMD misura la seconda linea e Arm resta beta architetturale.AI Semis

- ORCL— Oracle resta la lezione sul capex AI. Il mercato ama backlog cloud e domanda AI, ma continua a chiedersi quanto debito, capex e free cash flow negativo siano accettabili in cambio della crescita infrastrutturale.AI Capex

- DELL / HPE / SMCI— I server AI restano il checkpoint della domanda reale. Il mercato vuole ordini, margini, backlog convertito e deployment enterprise, non soltanto narrativa.AI Servers

- VRT / ETN / GEV— Power e cooling restano letture strutturali dell’infrastruttura AI. Data center, elettricità, sottostazioni, raffreddamento e backup power sono il lato più concreto del secondo ordine AI.Power / Cooling

- AAPL / ADBE— Apple resta sotto lente AI consumer e regolazione europea, mentre Adobe misura se il software viene ancora premiato per la monetizzazione AI quando emergono dubbi sull’esecuzione.Tech Quality

- NVO / LLY— Novo Nordisk ed Eli Lilly restano la coppia leader nei GLP-1. Il mercato segue formulazioni orali, capacità produttiva, accesso, pricing, tollerabilità e difesa del moat competitivo.Obesity Drugs

- COGT— Cogent resta una storia post-EHA da monitorare. I dati APEX su bezuclastinib in mastocitosi sistemica avanzata hanno dato al mercato un catalyst concreto; ora contano qualità della reazione, timing NDA e durata della narrativa clinica.EHA / Data

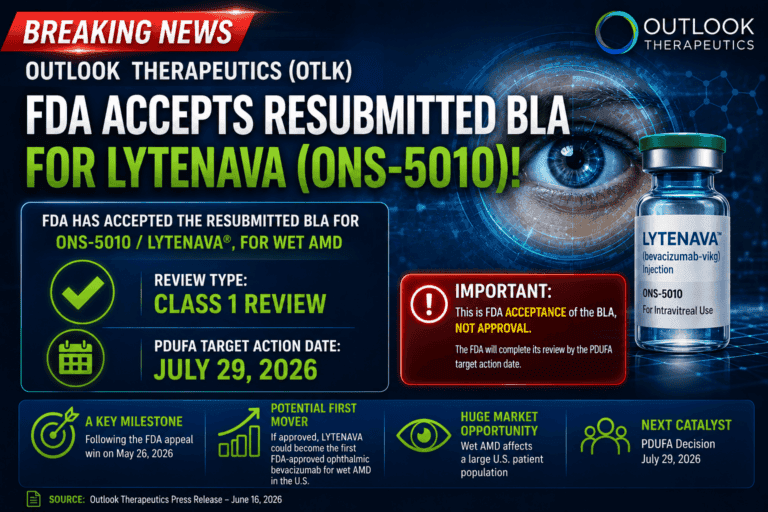

- VRDN— Viridian resta uno dei catalyst biotech più chiari di fine giugno, con veligrotug in Priority Review FDA e PDUFA target date al 30 giugno 2026 per thyroid eye disease.PDUFA Watch

- GILD / MRK / PHAR— Gilead e Merck restano rilevanti per la terapia HIV orale settimanale islatravir/lenacapavir, mentre Pharming mantiene un calendario FDA definito con PDUFA 24 ottobre 2026 per Joenja/leniolisib pediatrico in APDS.Biotech

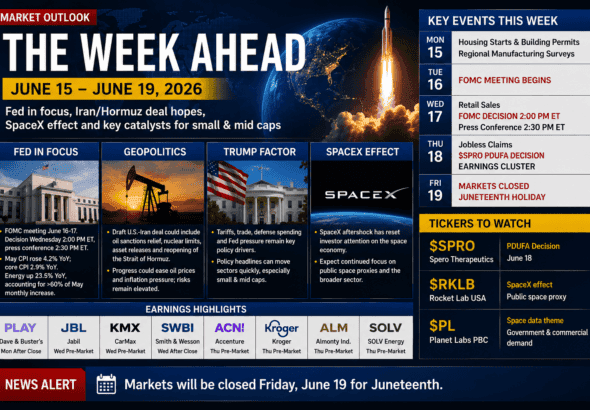

- Fed decision day— Il 17 giugno è il vero gatekeeper macro. Il mercato si aspetta una Fed ferma sui tassi, ma statement, proiezioni e conferenza stampa di Kevin Warsh possono determinare se il rally si allarga o si blocca.Fed

- Petrolio sotto $80— Brent sotto $80 aiuta la psicologia dell’inflazione e sostiene obbligazioni e azionario, ma il mercato deve ancora verificare supply iraniana, tempistiche, Hormuz e credibilità politica dell’accordo.Oil

- Hormuz resta il test pratico— Rotte navali, assicurazioni, sicurezza, backlog e normalizzazione fisica dei flussi contano più degli slogan politici. È lì che il trade sul petrolio verrà confermato o smentito.Shipping

- Dollaro più difensivo— Il dollaro è meno sostenuto dal safe haven perché l’accordo USA-Iran ha ridotto la paura immediata. Ma se Warsh sorprende in modo hawkish, il dollaro può tornare rapidamente centrale.FX

- Tech deve confermare— Dopo una fase più debole per Nasdaq e semiconduttori, il mercato deve capire se la pressione tech è semplice rotazione o deterioramento del risk appetite.Tech

- Settimana di scadenze— Triple witching, settimana USA accorciata, opzioni SpaceX, Fed e ribilanciamenti S&P aumentano la probabilità di swing intraday anche se la narrativa macro resta costruttiva.Volatility

Daily Briefing – June 17: Fed Decision Day, Oil Below $80, SpaceX Becomes a Volatility Machine, MRVL/FLEX Stay in the S&P 500 Flow Window, and Europe Follows the U.S. Signal

The June 17 briefing keeps the main focus on the United States because today’s global tape is built around the Federal Reserve decision. Oil remains below $80 after the U.S.–Iran framework and reports of possible sanctions relief for Iranian crude, but the market still needs confirmation from Hormuz shipping, insurance, physical flows and political follow-through. SpaceX is no longer just the record IPO story: with options now central to the trade, SPCX has become a direct gauge of volatility, retail demand, gamma and high-beta risk appetite. Marvell and Flex remain important technical catalysts ahead of their scheduled S&P 500 additions before the June 22 open. For Italy and Europe, the key question is whether lower crude and lower geopolitical stress can support banks, industrials, travel, defence and selected semiconductor exposure while still following the broader U.S. macro signal.

- SPCX— SpaceX remains the market’s cleanest retail-risk thermometer. After the record Nasdaq debut, the stock has moved from a simple IPO narrative into a valuation, float, momentum and demand-digestion story. The key question is not only whether price can rise, but whether volatility remains manageable.Space IPO

- SPCX Options— SpaceX options add a major mechanical layer. Heavy call demand can support momentum, but the same flows can also create violent reversals when hedging, gamma and intraday liquidity shift.Options

- RKLB / LUNR / PL / SATL— The public space basket remains in a post-SpaceX verification phase. SpaceX validates the theme, but it does not automatically validate every listed space name. RKLB, LUNR, PL and SATL need independent relative strength, not only headline sympathy.Space Basket

- MRVL / FLEX— Marvell and Flex remain real technical catalysts because S&P Dow Jones Indices has scheduled both additions to the S&P 500 for June 22, 2026. The setup is about passive demand, ETF rebalancing, benchmark flows, liquidity and positioning.Index Flow

- MRVL— Marvell has the stronger narrative inside the rebalance pair because it combines S&P 500 inclusion, custom silicon, data-center networking and second-layer AI infrastructure exposure. The test is whether investors still want AI exposure beyond the mega-cap leaders.AI / Index

- FLEX— Flex brings the industrial-technology and electronics-manufacturing side of the rebalance. It is less flashy than Marvell, but still relevant for supply chains, AI hardware, manufacturing capacity and benchmark-driven demand.Industrial Tech

- NVDA— Nvidia remains the anchor of the AI trade. If NVDA holds, AI can continue to act as the market’s leadership spine. If it weakens into Fed day, secondary AI names become more vulnerable.AI Leader

- AVGO / MRVL / AMD / ARM— AI semiconductor breadth remains one of the most important checks. Broadcom is the custom-silicon benchmark, Marvell adds the index-flow layer, AMD tests second-line appetite and Arm remains architecture beta.AI Semis

- ORCL— Oracle remains the AI capex lesson. The market likes cloud backlog and AI demand, but investors are still asking how much capex, debt and negative free cash flow should be tolerated in exchange for infrastructure growth.AI Capex

- DELL / HPE / SMCI— AI server names remain the real-demand checkpoint. The market wants orders, margins, backlog conversion and enterprise deployment, not only narrative momentum.AI Servers

- VRT / ETN / GEV— Power and cooling remain structural AI infrastructure reads. Data centers, electricity, substations, thermal management and backup power are among the most concrete second-order AI themes.Power / Cooling

- AAPL / ADBE— Apple remains under the consumer-AI and European regulatory lens, while Adobe tests whether software investors still reward AI monetization stories when execution questions appear.Tech Quality

- NVO / LLY— Novo Nordisk and Eli Lilly remain the GLP-1 leadership pair. The market is focused on oral formulations, manufacturing capacity, access, pricing, tolerability and the durability of the competitive moat.Obesity Drugs

- COGT— Cogent remains a post-EHA follow-through story. The APEX data for bezuclastinib in advanced systemic mastocytosis gave the market a defined clinical catalyst; now the focus shifts to reaction quality, NDA timing and durability of the data narrative.EHA / Data

- VRDN— Viridian remains one of the cleanest late-June biotech catalyst watches, with veligrotug under FDA Priority Review and a June 30, 2026 PDUFA target date in thyroid eye disease.PDUFA Watch

- GILD / MRK / PHAR— Gilead and Merck remain relevant for once-weekly oral islatravir/lenacapavir in HIV, while Pharming keeps a defined FDA calendar with an October 24, 2026 PDUFA date for pediatric Joenja/leniolisib in APDS.Biotech

- Fed decision day— June 17 is the macro gatekeeper. The market expects the Fed to stand pat, but the statement, projections and Kevin Warsh’s press conference can decide whether the rally broadens or stalls.Fed

- Oil below $80— Brent below $80 helps inflation psychology and supports bonds and equities, but the market still needs to verify Iranian supply, timing, Hormuz and the political credibility of the deal.Oil

- Hormuz remains the practical test— Shipping routes, insurance, safety assurances, backlog clearance and physical flow normalization matter more than political slogans. That is where the oil-relief trade will be confirmed or rejected.Shipping

- Dollar turns more defensive— The dollar has lost some safe-haven support as the U.S.–Iran agreement reduced immediate fear. But if Warsh surprises hawkishly, the dollar can quickly return to the center of the tape.FX

- Tech needs confirmation— After a softer phase for Nasdaq and semiconductors, the market needs to know whether tech pressure is simple rotation or broader deterioration in risk appetite.Tech

- Expiration week mechanics— Triple witching, a shortened U.S. week, SpaceX options, Fed risk and S&P 500 rebalancing increase the probability of intraday swings even if the macro narrative remains constructive.Volatility